How Developers Can Benefit from Bridge Loans

Summary

Learn how bridge loans for developers offer fast, flexible funding for projects with short timelines and unique financing needs.

Navigating Development Financing Gaps

Bridge loans for developers are short-term financing solutions designed to help real estate developers fund projects during critical transition periods. They typically last 6-36 months and serve as interim funding until permanent financing or project completion.

What Are Bridge Loans for Developers?

| Feature | Description |

|---|---|

| Purpose | Short-term financing that "bridges" gaps between development phases |

| Loan Amount | Typically 60-80% of project cost (up to 90% for experienced developers) |

| Interest Rates | 6-15% (higher than conventional loans but with faster approval) |

| Term Length | 6-36 months (most commercial bridge loans under 3 years) |

| Closing Speed | As quick as 3-7 days with hard money lenders vs. weeks/months for traditional financing |

| Payment Structure | Usually interest-only during the loan term |

| Exit Strategy | Required - typically refinancing or property sale |

Bridge loans provide crucial flexibility for developers facing time-sensitive opportunities. Whether you need to quickly secure land, begin construction before permanent financing is in place, or renovate a property for repositioning, bridge loans offer speed and adaptability that traditional bank financing can't match.

The key advantage is timing - while conventional lenders might take months to approve construction loans, bridge lenders can often fund within days or weeks. This speed comes at a premium through higher interest rates and fees, but the ability to seize opportunities quickly often justifies the cost.

I'm Zakary Fouladi, and I've helped developers structure bridge loans for projects ranging from multifamily renovations to ground-up construction, specializing in creating flexible bridge loans for developers that maximize leverage while preserving exit options. My approach focuses on aligning short-term bridge financing with long-term project goals.

Must-know bridge loans for developers terms:- real estate development loans- debt service coverage ratio loan- private money lending

Why Speed Matters in Development

In real estate development, timing can make or break a project. Market opportunities don't wait for traditional bank approvals, and competitors with ready capital can swoop in while you're still gathering documentation for conventional financing.

Consider this scenario: A prime parcel of land becomes available in a rapidly appreciating neighborhood. The seller needs to close within 30 days. Traditional construction loans might take 60-90 days for approval, but a bridge loan can fund in as little as 7-14 days. That speed difference could be the deciding factor in securing the property.

"When a developer seeks to finance their project with historic tax credit equity, they will find only a portion of the equity will be contributed during construction, with the remaining amount contributed after the development is placed in service," notes a leading tax credit advisor. This timing gap is where bridge financing becomes essential.

Auction deadlines present another time-sensitive scenario. Properties sold at auction typically require funding within 30 days or less. A bridge loan's accelerated timeline makes it possible to participate in these opportunities that would otherwise be inaccessible with conventional financing.

Who This Guide Serves

This guide is designed for developers across various project types:

- Ground-up developers seeking to acquire land and begin construction before securing permanent financing

- Value-add investors looking to purchase and renovate underperforming properties

- Land acquisition specialists needing quick capital to secure parcels for future development

- Rehabilitation project managers working on historic or adaptive reuse developments

Whether you're an experienced developer with multiple completed projects or a newer entrant to development with a strong business plan, understanding bridge loans can help you steer financing gaps and capitalize on opportunities that might otherwise be missed.

Bridge Loans for Developers 101

Think of a bridge loan as exactly what the name suggests - a financial bridge that gets you from one side of a project to the other. When you're developing real estate, timing gaps between phases can create real headaches. That's where bridge loans for developers shine.

These loans aren't designed to be your forever financing. They're the trusty sidekick that helps you through the tricky middle parts of your development journey - typically lasting anywhere from 6 months to 3 years before you transition to something more permanent.

What are bridge loans for developers?

Bridge loans for developers are essentially your financial first responders. When you need capital quickly to seize an opportunity, these short-term, asset-based loans step in to save the day. Unlike traditional financing that might scrutinize your tax returns for months, bridge lenders focus primarily on the property's value and your exit strategy.

These loans serve as critical gap-funding tools when you're:- Snagging a property before you have all your entitlements in hand- Covering those often-overlooked predevelopment costs before your construction loan closes- Funding renovations on a property that doesn't yet qualify for permanent financing- Keeping your project afloat during that nail-biting lease-up period

Most bridge loans for developers are secured by a first-lien position on your property. This gives the lender confidence they can recover their investment if things go sideways. Second-lien bridge loans exist too, but expect higher interest rates and lower leverage since the lender is taking on more risk.

I recently spoke with a developer in Chicago who told me, "When we found that abandoned warehouse, we knew it would be perfect for apartments, but our bank wanted six weeks for approvals. The bridge lender looked at the property, loved our conversion plans, and funded in just 10 days. That speed made all the difference."

How do bridge loans for developers work?

The beauty of bridge financing is its simplicity compared to traditional construction loans. Here's the real-world process:

When you apply, lenders evaluate your project using metrics like LTV (loan-to-value), LTC (loan-to-cost), and sometimes ARV (after-repair value). Your personal credit matters, but not nearly as much as with conventional financing. What really counts is the property's potential and your clear plan for repaying the loan.

The draw schedule tends to be more flexible than with construction loans. Rather than tying every dollar to specific milestones and inspections, you'll often receive more funds upfront with a simpler structure for subsequent draws. This flexibility can be a godsend when project timelines shift.

Hard-money and non-bank lenders dominate this space because they're built for speed. While your local bank might need 60+ days to approve financing, these specialized lenders can often fund in as little as 3-7 days. Yes, you'll pay more in interest, but when time is money, the math often works in your favor.

Most bridge loans feature interest-only payments during the term, preserving your cash flow for the actual development work. Many lenders will even build in interest reserves, setting aside a portion of the loan proceeds specifically to make those interest payments.

The underwriting process feels noticeably different from traditional financing. Rather than diving deep into your personal finances, bridge lenders focus on the collateral value and the feasibility of your exit strategy. This asset-based approach means even developers with credit challenges can secure funding if their project fundamentals are strong.

As one experienced developer put it, "Bridge loans aren't about where you've been financially—they're about where this specific project is going." That mindset is why bridge loans for developers have become such a vital tool in today's fast-moving real estate market.

Remember though - every bridge loan needs a clear exit strategy, whether that's refinancing with permanent debt once your project stabilizes or selling the completed development. The lender will want to understand exactly how you plan to repay them before they hand over the funds.

When & Why Developers Use Them

Developers turn to bridge loans in various scenarios where traditional financing falls short or timing constraints demand faster solutions. Understanding when these loans make sense can help you determine if they're right for your project.

Common Project Types

The beauty of bridge loans for developers is their versatility across multiple project types. Let me walk you through some common scenarios where they shine:

Ground-up multifamily development often faces a chicken-and-egg problem – you need to secure land and begin site work before a construction lender will commit. I recently worked with a Florida developer who solved this exact problem using a $2.4 million bridge loan to acquire land and complete initial site work for a 30-unit apartment complex. This gave them breathing room to finalize their construction loan without losing the opportunity.

Office repositioning projects are another perfect fit. Imagine finding an outdated office building with great bones but terrible finishes. A Manhattan developer I know secured a $5.6 million bridge loan to acquire and renovate a Class B office building, completing the change in just 9 months. Once the building sparkled with modern amenities, they refinanced with permanent financing at a much lower rate.

The e-commerce boom has created fascinating opportunities in industrial conversion. "We used a $3.2 million bridge loan to acquire a vacant warehouse and begin renovations while we secured tenants," one developer shared with me. "Once we hit 60% pre-leasing, we refinanced with a permanent loan at a much lower rate." This approach let them move quickly when the property became available without waiting for leasing to begin.

Subdivision development presents unique cash flow challenges that bridge loans address beautifully. A Texas developer recently used bridge financing to fund infrastructure work on a 45-lot subdivision, then methodically repaid the loan as finished lots sold to homebuilders. The bridge loan carried the project through the value-creation phase until revenues began flowing.

Historic Tax Credit (HTC) projects have their own financing quirks that bridge loans solve neatly. According to recent research on HTC financing, "Only 25% of HTC equity is typically available at closing, leaving 75% to be bridged until project milestones are met." Most bridge lenders will advance 90-95% of anticipated future tax credit equity, filling this critical gap.

Advantages

The magic of bridge loans for developers comes from several key advantages:

Fast closing tops the list for most developers I work with. While traditional construction loans often take 60-90 days to close, bridge loans can fund in as little as 3-7 days with hard money lenders, or 2-3 weeks with private lenders. This speed difference can be the deciding factor when sellers want quick closings or auction deadlines loom.

Flexible terms are another huge benefit. Unlike conventional loans with rigid structures, bridge lenders can customize almost everything to match your specific project needs – interest reserves that cover payments during construction, flexible draw schedules that align with your project timeline, or extension options that provide peace of mind if unexpected delays occur.

Interest-only payments preserve precious cash flow during development. Most bridge loans require only interest payments during the loan term, which means more of your capital stays in the project when the property isn't generating income. This structure aligns perfectly with development timelines.

Higher leverage options exist for experienced developers. While conventional construction loans might cap at 65-70% loan-to-cost, bridge loans typically fund 60-80% of project costs, with some lenders offering up to 90% LTC for developers with strong track records. This higher leverage means you can stretch your equity further across multiple projects.

The streamlined documentation requirements save valuable time. Bridge lenders focus primarily on the property and exit strategy rather than demanding mountains of personal financial documentation. This practical approach gets deals done faster.

Disadvantages

I always make sure my clients understand the trade-offs with bridge financing:

Higher interest rates are the most obvious drawback. Rates typically range from 6% to 15% – significantly higher than conventional financing. This premium reflects the increased risk the lender takes and the shorter term of the loan. While the rate might make you wince, remember to calculate the actual dollar cost over the expected holding period, not just the rate itself.

Substantial fees come with the territory. Origination fees typically range from 1% to 3% of the loan amount, plus you may face additional points, processing fees, and due diligence expenses. These upfront costs impact your overall returns, so factor them into your project analysis.

Short maturity risk creates pressure to execute your plan efficiently. With terms typically ranging from 6-36 months, you face refinancing risk if market conditions change or project timelines extend beyond expectations. A Chicago developer recently cautioned me: "We used a bridge loan for a mixed-use project, but construction delays pushed us beyond our initial term. The extension fees and higher interest rate during the extension period significantly impacted our returns."

Default penalties tend to be stricter than with conventional loans. Bridge loans often include tough default provisions, which can include higher default interest rates, additional fees, or accelerated repayment requirements. Make sure you understand these terms thoroughly before signing.

The right bridge loan can be the difference between seizing an opportunity and watching it pass by. At BrightBridge Realty Capital, we specialize in creating bridge financing solutions that align with your development timeline and exit strategy. Our approach focuses on understanding your specific project needs rather than forcing you into a one-size-fits-all product. For more context on the evolving bridge loan landscape, check out the latest research on bridge financing.

Terms, Costs, and Underwriting Essentials

Let's talk money – because when it comes to bridge loans for developers, understanding the dollars and cents is crucial before diving in. Having funded hundreds of projects, I've seen how these numbers can make or break a development plan.

When developers call me about bridge financing, their first question is usually about interest rates. Truthfully, bridge loan rates typically range from 6% to 15% – and yes, that's higher than conventional financing. The exact rate depends on your project's risk profile, your track record, location, and current market conditions. Think of this premium as the cost of speed and flexibility.

Beyond the rate, you'll encounter several fees that impact your total cost. Origination fees typically run 1-3% of the loan amount. Many lenders also charge points (each point equals 1% of the loan amount), extension fees if you need more time (usually 0.25-1% per extension), and sometimes exit fees of 1-2% when you repay the loan.

One developer client recently told me, "I was shocked by the extension fee when construction delays pushed my timeline back three months – but in hindsight, the flexibility was worth every penny compared to defaulting on a conventional loan."

Leverage is another crucial factor. For commercial properties, expect loan-to-value (LTV) ratios of 65-75%, though this can stretch to 80% for compelling value-add opportunities. Residential projects typically qualify for 70-80% LTV. If you're looking at loan-to-cost (LTC) metrics, most bridge lenders offer 70-90% depending on your experience and project type.

Speaking of experience – your track record matters. Most bridge lenders prefer borrowers with credit scores above 680, a history of successful similar projects, and financial strength. You'll typically need a net worth equal to or exceeding the loan amount and liquidity of 10-20% of what you're borrowing.

The standard term length for these loans runs 6-36 months, with most falling in the 12-24 month range. Many lenders offer extension options of 6-12 months, though these come with additional fees.

Key Documents Lenders Require

When I work with developers on bridge financing, I always emphasize being prepared with the right paperwork. Bridge lenders may be faster than banks, but they still need to verify your project's viability.

On the project side, come prepared with your pro-forma financial projections that show expected returns, a detailed construction budget with schedule of values, architectural plans, relevant permits (or evidence you're in the entitlement process), environmental reports, and a property appraisal showing both as-is and as-completed values.

For borrower documentation, you'll need your personal financial statement, a schedule of real estate owned (your portfolio), a resume highlighting development experience, a solid business plan with clear exit strategy, your entity formation documents, and tax returns for both you and your business.

As one veteran developer shared with me, "The strength of your exit strategy is often the most important factor in bridge loan approval. Lenders want to see a clear, realistic plan for repayment through refinancing or sale."

Special Situations: Historic Tax Credit Bridging

Historic Tax Credit (HTC) projects present unique financing challenges that bridge loans are perfectly positioned to solve. If you've ever tackled a historic renovation, you know the funding timing can be maddening.

The core issue is that only about 25% of HTC equity is typically available at closing, with the remaining 75% contributed after project completion and certification. This creates a significant cash flow gap during construction – precisely what bridge financing addresses.

Specialized HTC bridge lenders will typically advance 90-95% of anticipated future tax credit equity, allowing you to access nearly all of the tax credit value upfront. One clever advantage: the interest and loan fees on HTC bridge loans qualify as Qualified Rehabilitation Expenditures (QREs), making them eligible for tax credits themselves. This can offset 13-17% of interest costs for federal credits, and potentially 30%+ when state HTCs are available.

As noted in external research on HTC financing, "When a developer seeks to finance their project with HTC equity, they will find only a portion of the equity will be contributed during construction, with the remaining amount contributed after the development is placed in service."

I recently worked with a developer converting a 1920s warehouse into mixed-use space, and the HTC bridge loan made the difference between the project happening or sitting idle for another year. By bridging 92% of the anticipated tax credits, we closed a $1.2 million funding gap that no conventional lender would touch.

How to Secure and Repay Your Bridge Loan

The journey to securing a bridge loan moves at a much faster pace than traditional financing. Let's walk through what you can expect when applying for bridge loans for developers and how to successfully steer the repayment process.

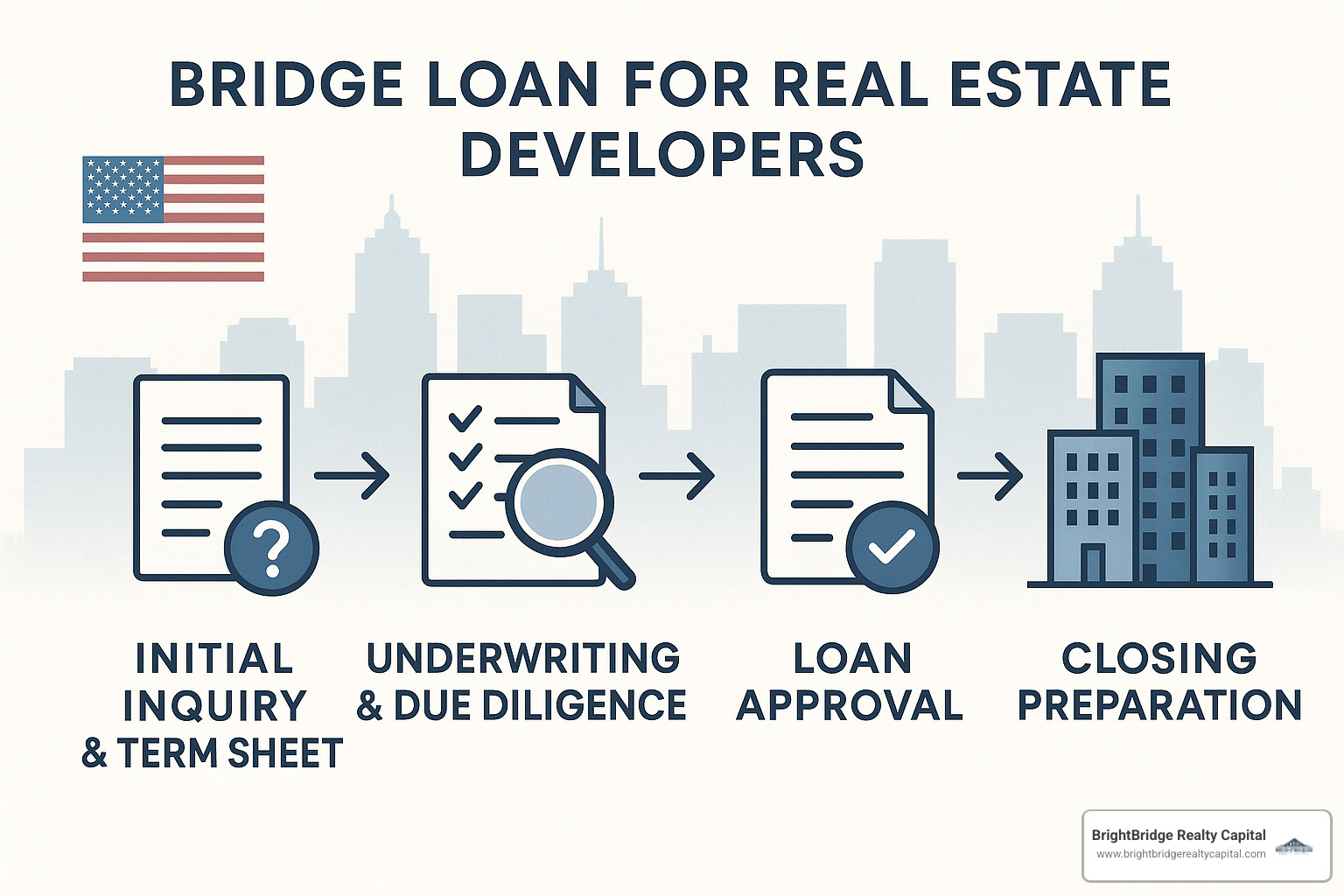

From first contact to funding, the entire bridge loan process typically takes between 3-21 days – a dramatic improvement over the 60-90 day timeline for conventional construction loans. Here's the typical journey:

First, you'll receive a term sheet within 1-3 days of your initial inquiry. The lender then dives into underwriting and due diligence, which usually takes 2-10 days. After a quick 1-2 day approval process, you'll spend 1-5 days preparing for closing, followed by funding in just 1-2 days.

I recently worked with a developer in New York who shared: "We had a term sheet in our hands 24 hours after applying. Ten days later, we closed the loan. That speed made all the difference – we were up against all-cash buyers and would have lost the property without the quick funding."

The closing process itself involves property appraisal (though this is sometimes waived for lower LTV loans), title search and insurance, environmental review (often just a Phase I), legal documentation, and recording the collateral.

Boosting Approval Odds

Want to improve your chances of getting approved for a bridge loan for developers with favorable terms? Focus on these key areas:

Develop a Strong Exit Plan that clearly outlines how you'll repay the loan. Whether through refinancing or property sale, include market comparables, realistic timelines, and thoughtful contingency plans. As one experienced bridge lender told me, "We're looking for developers who've thought beyond just the primary repayment strategy – we want to see Plan B and even Plan C if market conditions shift."

Offer Additional Collateral if your project's LTV ratio is on the borderline. This might be other properties you own, personal guarantees, or cross-collateralization. This simple step can significantly improve your loan terms.

Build a Realistic Contingency Budget that includes a 10-15% buffer for unexpected costs. This demonstrates to lenders that you understand project risks and are planning accordingly. Nobody likes surprises – especially not lenders!

Conduct DSCR Stress Tests even though bridge loans typically feature interest-only payments. Lenders want confidence that your completed project will generate enough cash flow to support permanent financing. Run these tests at varying occupancy levels and interest rates to show you've considered multiple scenarios.

Demonstrate Experience with similar projects whenever possible. If you're newer to development, consider partnering with seasoned developers or bringing experienced team members onto your project. Lenders feel more comfortable when they see a track record of success.

Planning the Exit

The exit strategy is the most critical component of any bridge loan application. Here are the most common approaches to successfully repaying your bridge loans for developers:

Refinance to Permanent Financing once your project reaches stabilization. This is the most common exit path, with several options available:

HUD/FHA loans offer excellent leverage and long terms for multifamily properties. CMBS loans provide non-recourse financing for stabilized commercial properties. Agency loans through Fannie Mae or Freddie Mac work well for qualified multifamily projects. And traditional bank financing becomes available once your property meets income requirements.

One financing specialist I work with regularly explains, "Bridge-to-HUD financing is particularly valuable for multifamily developers. The bridge loan covers construction and lease-up, then seamlessly transitions to long-term, fixed-rate HUD financing after the property stabilizes."

Property Sale works well for fix-and-flip or merchant build strategies. Your exit comes through selling the completed project, which requires accurate market analysis, realistic pricing, a solid marketing plan, and a contingency timeline if the sale takes longer than anticipated.

Rental Stabilization is crucial for value-add projects. Achieving target occupancy and rental rates qualifies your property for permanent financing. Lenders want to see market-supported lease-up projections, a thoughtful marketing strategy, a solid property management plan, and break-even occupancy analysis.

A developer client in Los Angeles recently shared their success story: "We used a bridge loan to buy and renovate a 40-unit apartment building that was only 60% occupied. After completing renovations and reaching 92% occupancy, we refinanced with a 30-year fixed-rate loan that paid off the bridge debt and even returned some of our equity."

At BrightBridge Realty Capital, we specialize in creating customized bridge loans for developers with clear exit strategies. Our team can often close within a week, offering direct lending without intermediaries for a smoother, faster process. We understand that in development, timing is everything – and our competitive rates combined with flexible terms can help you seize opportunities that might otherwise slip away.

Frequently Asked Questions about Bridge Loans for Developers

How much can a developer borrow?

When developers ask me this question, I always tell them the same thing: it depends on your project, your experience, and the property itself. Bridge loans for developers offer flexible funding, but lenders still have their limits.

For most commercial properties, you're looking at 65-75% of the property value, while residential projects might stretch to 80%. If you're working with a special-use property (like a hotel or specialized industrial facility), expect slightly lower limits around 60-70%.

Your experience makes a big difference too. Seasoned developers with successful track records can often secure 75-90% of total project costs, while those newer to development might be limited to 65-75%. Renovation projects typically qualify for higher leverages (75-85%) compared to ground-up construction (70-80%).

Lenders want to see you have meaningful "skin in the game." This usually translates to contributing 10-35% of total project costs from your own resources. Most will also check that you have liquidity equal to at least 10% of the loan amount and a net worth matching or exceeding what you're borrowing.

I spoke with a bridge loan specialist who works extensively with historic properties who told me: "For historic tax credit projects, we'll typically advance up to 90-95% of anticipated future tax credit equity, but we won't lend against future contributions that depend on the project reaching stabilization."

How fast can a bridge loan close?

Speed is where bridge loans truly shine. While conventional bank loans might keep you waiting for months, bridge financing can move at lightning pace.

Hard money lenders often close in just 3-7 days. They accomplish this through simplified underwriting and minimal documentation requirements. You'll pay for this speed with higher rates and fees, and they typically want you at the closing table in person.

Private lenders strike a nice middle ground, usually closing within 7-14 days. Their underwriting is more thorough than hard money but still streamlined compared to banks. Documentation requirements are reasonable, and many offer competitive rates for bridge financing. Some even provide remote closing options for added convenience.

Institutional bridge lenders typically take 14-30 days to close. They conduct comprehensive underwriting and require substantial documentation, but they offer the most competitive rates and terms. They're also usually comfortable with larger loan amounts for major development projects.

A capital markets advisor I work with regularly puts it well: "Bridge loans are among the fastest-closing financing packages available to commercial real estate borrowers. When all documentation is in order and the deal is straightforward, some loans can close in a matter of days."

At BrightBridge Realty Capital, we've streamlined our process to complete closings within a week for qualified borrowers who have their documentation ready.

What happens if market conditions shift?

This is a question that keeps developers up at night – and for good reason. Market shifts during a bridge loan term can create real challenges, but there are several ways to protect yourself.

Extension options are your first line of defense. Most bridge loans include provisions for extending the loan term (typically by 6-12 months) if your project timeline stretches beyond initial expectations. These extensions usually require paying a fee (0.25-1% of the loan amount), staying compliant with loan covenants, and showing clear progress toward your exit strategy.

For floating-rate bridge loans, consider purchasing interest rate caps. These financial tools set a maximum interest rate for your loan term, providing payment certainty even if rates climb. They're essentially insurance against dramatic rate increases.

Smart developers always create multiple exit scenarios. Your primary plan might be refinancing with permanent debt, but you should also have a secondary strategy (perhaps bringing in equity partners) and a fallback option (selling the property) if conditions change dramatically.

One veteran developer I've worked with for years shared this wisdom: "Always build time contingencies into your development schedule. If you think a project will take 12 months, secure an 18-24 month bridge loan term to give yourself buffer for unexpected delays."

This advice has saved countless projects from default when construction delays, permitting issues, or market shifts extended project timelines beyond original estimates.

Conclusion

Bridge loans for developers offer a powerful financing tool that provides speed, flexibility, and strategic advantages in the competitive real estate development landscape. While they carry higher costs than conventional financing, the ability to move quickly and structure terms around project-specific needs often justifies the premium.

At BrightBridge Realty Capital, we specialize in providing seamless, direct bridge lending with closings often completed within a week. Our competitive rates and customized solutions are designed to help developers capitalize on opportunities that traditional financing might miss due to timing constraints.

The key to successful bridge loan utilization isn't complicated, but it does require careful planning. Having a clear exit strategy is absolutely essential - whether through refinancing, sale, or other means, you need to know exactly how you'll repay the loan before you take it. I've seen too many developers focus solely on the acquisition without mapping out their endgame.

You'll also want to thoroughly understand the total costs involved. Those interest rates and fees can add up quickly! Factor in all interest, origination fees, and potential extension costs when evaluating whether your project pencils out. A bridge loan that helps you secure an amazing deal can be worth every penny of its premium pricing.

Smart developers always build in contingencies. Let's be honest - when was the last time a construction project finished exactly on schedule? Market conditions shift, construction timelines stretch, and leasing velocities rarely match our optimistic projections. Building buffers into your timeline and budget isn't pessimistic - it's realistic.

Finally, working with experienced lenders makes all the difference. Partner with lenders who truly understand development and can provide flexible solutions when challenges arise. The right lender becomes a partner in your success, not just a source of capital.

As one of our clients recently told me: "Bridge loans aren't just about getting from point A to point B. They're about creating opportunities that wouldn't exist without fast, flexible capital. Yes, they cost more, but the ability to secure deals that others can't is worth the premium."

For developers looking to move quickly on opportunities, steer financing gaps, or maximize leverage during critical project phases, bridge loans remain an essential tool in the development financing toolkit. They're not right for every situation, but when conventional financing is too slow or restrictive, a well-structured bridge loan can be the difference between watching an opportunity pass by and seizing it with both hands.

To learn more about how BrightBridge Realty Capital can help structure bridge financing for your next development project, contact our team today. We'd love to hear about what you're building next.