Funding Your Connecticut Real Estate Investments Made Easy

Summary

Discover connecticut property investment loans, compare options, and learn how to qualify for fast, affordable funding in Connecticut.

Why Connecticut Property Investment Loans Are Your Gateway to Real Estate Success

Connecticut property investment loans offer real estate investors a pathway to capitalize on one of the Northeast's most stable and accessible markets. With median home prices below neighboring states and strong rental demand in college towns like New Haven, Connecticut presents compelling opportunities for both fix-and-flip projects and buy-and-hold investments.

Quick Answer: Connecticut Property Investment Loan Options

- Conventional Loans: 20-25% down, up to 80% LTV, rates 5.8-8.9%

- DSCR Loans: Qualify on property cash flow, 80% LTV, rates starting at 7.0%

- Hard Money: Close in 48 hours, rates 8.9-10.9%, up to 85% purchase + 100% rehab

- SBA Loans: Up to 90% LTV for qualified investors

- Portfolio Loans: Minimum $225K, consolidate 3+ properties

- Home Equity: Leverage existing property equity for new investments

Connecticut's rental market remains robust, particularly in areas near Yale University and other educational institutions. The state's relatively affordable entry points compared to New York and Massachusetts make it attractive for investors seeking steady cash flow and long-term appreciation potential.

I'm Daniel Lopez, a loan officer at BrightBridge Realty Capital with extensive experience helping investors steer Connecticut property investment loans across residential and commercial deals. My background in structuring creative financing solutions has helped clients secure funding for everything from single-family flips to multi-unit apartment acquisitions throughout the Constitution State.

Handy connecticut property investment loans terms:- connecticut construction loans- private funding for real estate investors- short term real estate loans

Mapping the Loan Landscape in Connecticut

Connecticut's investment property financing offers multiple options once you know where to look. The key is matching the right loan type to your specific investment strategy and timeline.

Conventional loans are the steady workhorses of real estate investing. These traditional bank products typically ask for 20-25% down payment and offer rates between 5.8% and 8.9%. They're reliable and perfect for buy-and-hold strategies when you have strong credit and documented income.

DSCR loans have completely changed the game for Connecticut property investment loans. Instead of scrutinizing your W-2s and tax returns, these lenders care about one thing: can the property pay for itself? With a debt service coverage ratio of 1.0 or higher, you can secure financing up to 80% LTV with 30-year terms.

When speed matters most, hard money and private loans become your best friends. We're talking 48-hour closings when everything's ready to go. Yes, you'll pay 10-12% rates with 2-5 points, but when you find that perfect flip property and need to move fast, these loans are worth their weight in gold.

FHA and VA loans open doors for house-hacking strategies. FHA lets you get into a multi-unit property with just 3.5% down if you live in one unit. VA loans offer 0% down for eligible veterans on properties up to four units.

For larger deals, SBA 7(a) and 504 loans can finance up to 90% of commercial investment properties. These government-backed programs shine for mixed-use properties or larger multifamily investments.

| Loan Type | Typical LTV | Down Payment | Interest Rate Range | Best For |

|---|---|---|---|---|

| Conventional | Up to 80% | 20-25% | 5.8-8.9% | Buy-and-hold rentals |

| DSCR | Up to 80% | 20% | 7.0-10.5% | Cash-flow properties |

| Hard Money | Up to 85% | 10-15% | 8.9-10.9% | Fix-and-flip projects |

| SBA | Up to 90% | 10% | 2.0-7.0% | Owner-occupied commercial |

| Portfolio | Up to 75% | 25% | Varies | Multiple properties |

Conventional vs. Government-Backed Choices

Conventional loans through Fannie Mae and Freddie Mac programs require 20-25% down payment but offer competitive rates and predictable terms. Lenders count up to 75% of projected rental income toward your qualification.

FHA loans create opportunities for house-hacking with just 3.5% down and owner-occupancy requirements. VA loans offer the most generous terms available - eligible veterans can finance up to a four-unit property with zero down payment, provided they occupy one unit.

Private & Hard Money Routes

When traditional banks say "no" or "not fast enough," private and hard money lenders step in with asset-based loans that focus on the property's value and potential rather than your personal financial situation.

The speed is incredible - 48-hour closings are possible when all parties come prepared. You'll pay 10-12% rates with 2-5 origination points, but missing out on a great deal costs much more than higher interest rates.

DSCR Loans: Cash-Flow Centric Financing

DSCR loans have revolutionized how investors think about qualification. Instead of proving you can afford another mortgage payment, you prove the property can afford its own mortgage payment.

The magic number is a DSCR of 1.0 or higher. Most lenders prefer seeing 1.25 DSCR for the best terms. With rates starting at 7.0% and 30-year terms available, these loans offer excellent long-term financing for cash-flowing properties without requiring W-2s or tax returns.

Qualifying for Connecticut Property Investment Loans

Getting approved for Connecticut property investment loans doesn't have to feel overwhelming. Understanding the core requirements puts you miles ahead of investors who wing it.

Your credit score is your first impression - most conventional lenders want to see at least 680, though some DSCR programs will work with scores as low as 620. Hard money lenders are often more forgiving, sometimes accepting scores around 600.

Loan-to-value ratios determine how much skin you need in the game. Conventional investment loans typically cap out at 80% LTV, meaning you'll need at least 20% down. DSCR loans often match this at 80%, while hard money lenders might stretch to 85% of the purchase price.

Debt-to-income ratios matter for conventional loans, with most lenders preferring to keep you under 45% DTI. But here's the kicker - they'll count up to 75% of your projected rental income toward qualification.

Cash reserves separate the serious investors from the dreamers. Most lenders require 2-6 months of mortgage payments sitting in your account for each investment property.

Down Payment Rules for Connecticut Property Investment Loans

Conventional loans stick to 20-25% down payment for investment properties. DSCR loans typically ask for 20% down, though strong cash-flowing properties might open doors to 15% down options.

Hard money and private lenders often require just 10-15% down, with the rest financed based on your total project costs. SBA loans offer as little as 10% down for qualified commercial investors. VA loans deliver zero down payment on properties up to four units for eligible veterans.

Documentation Checklist

Your personal financial picture starts with tax returns from the past two years, recent bank statements, and proof of income. Property-related documents include purchase contracts, appraisals, and rent rolls for existing rentals.

Business and legal documents matter when buying through an LLC. Lease agreements and rental history strengthen DSCR loan applications significantly. Insurance documentation protects your investment and satisfies lender requirements.

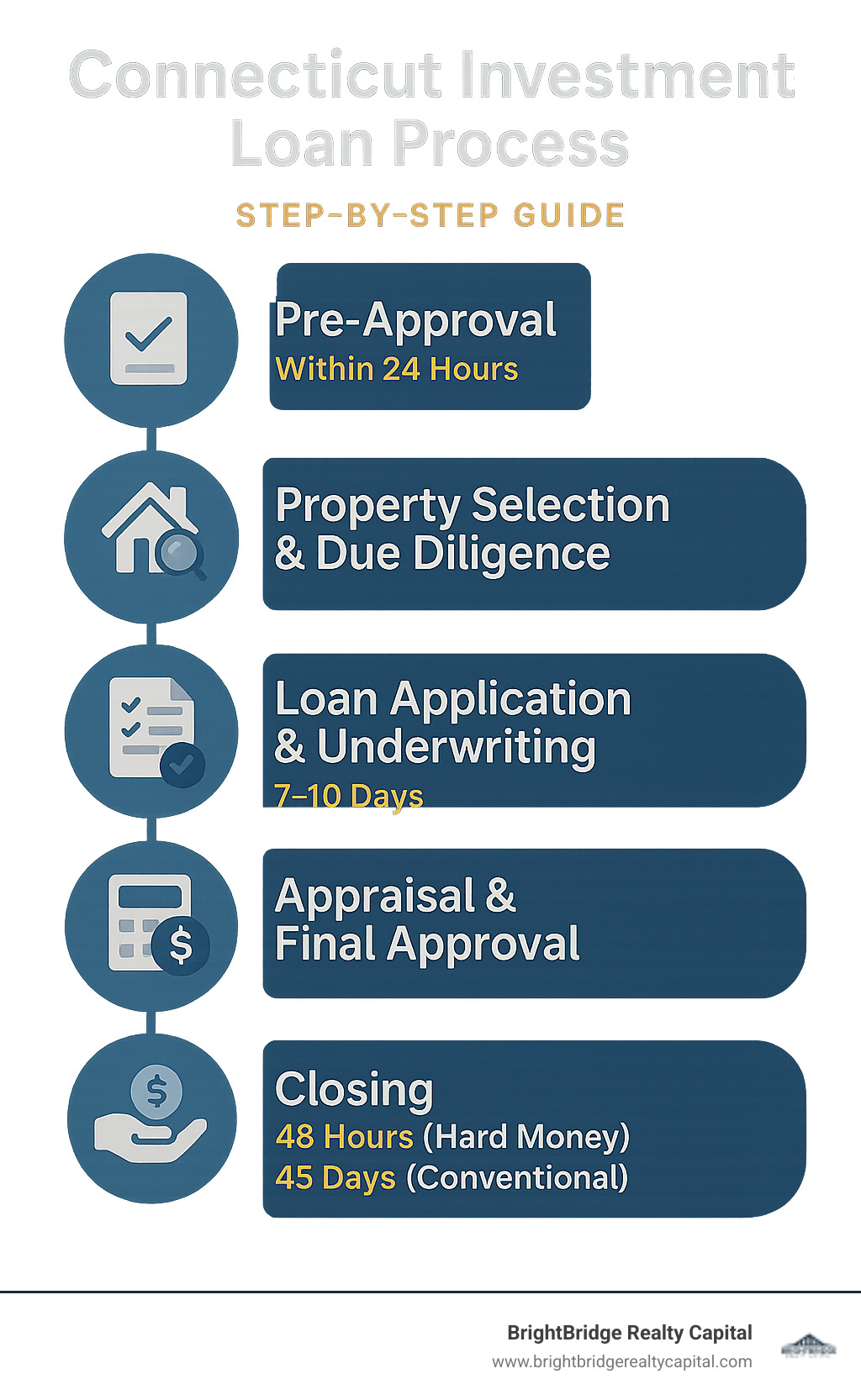

Application & Approval Timeline

Pre-approval happens within 24-48 hours for initial credit review. Full application submission takes 1-3 days with complete documentation. Underwriting review typically takes 7-10 days. The appraisal process runs 5-10 days. Final approval and closing wraps up in 3-5 days.

At BrightBridge Realty Capital, our direct lending model eliminates intermediaries, often allowing us to close within a week of final approval.

Advanced Strategies & State-Specific Programs

Connecticut's investment landscape offers sophisticated financing strategies that go beyond basic rental property loans.

Home Equity Lines of Credit (HELOCs) provide flexible access to capital as opportunities arise. The rates often beat hard money by several percentage points, and there's no prepayment penalty when you pay off the balance after closing on permanent financing.

Portfolio or blanket loans represent the next level for serious investors. Once you hit three properties and $225,000 in total loan amount, you can consolidate everything under one loan with single underwriting efficiency and cross-collateral benefits.

The BRRRR Method works exceptionally well in Connecticut's stable rental market. Buy, rehab, rent, refinance, and repeat with recycled capital. Connecticut's steady appreciation and strong rental demand make this strategy particularly reliable.

1031 exchanges offer ultimate tax-deferral for scaling your portfolio. Roll proceeds into larger properties without paying capital gains taxes.

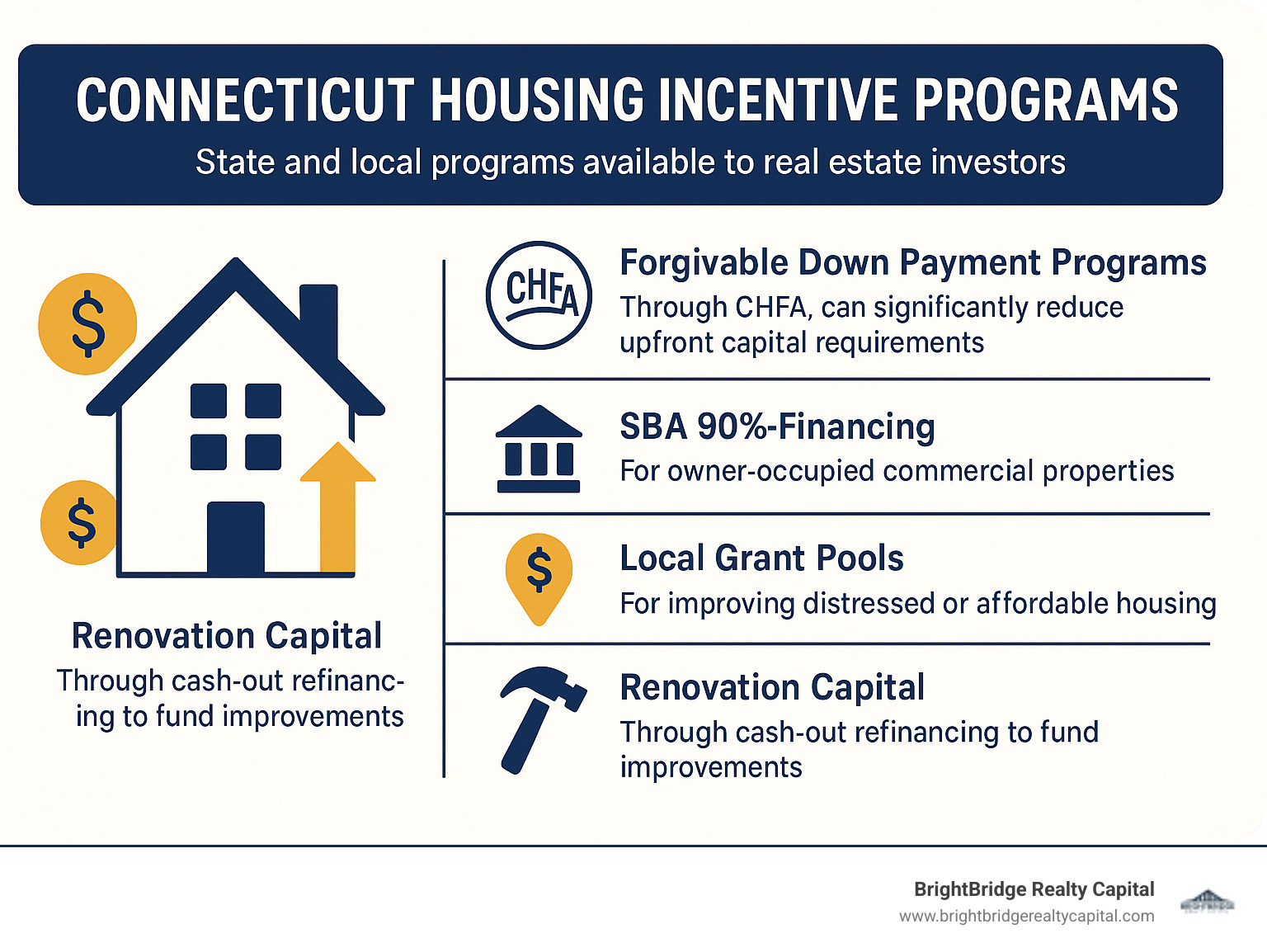

The Connecticut Housing Finance Authority (CHFA) creates unique opportunities for investors. In 2022 alone, CHFA approved financing for 1,619 units of affordable multifamily housing, totaling more than $350 million in development.

Leveraging DSCR & Portfolio Loans for Rapid Scaling

DSCR and portfolio loans become incredibly powerful for maximum impact. The single underwriting approach eliminates exhausting individual loan applications. Cross-collateral structuring lets your strongest properties support your entire portfolio.

DSCR portfolio combinations create the ultimate scaling tool - finance multiple properties based purely on their combined cash flow without personal income verification.

Cash-Out & HELOC Plays to Reinvest

Cash-out refinancing typically allows access to up to 75% of your property's current value. The tax-deferred advantage of refinancing versus selling cannot be overstated - access equity without immediate tax consequences.

HELOC flexibility provides ongoing access to capital as opportunities arise, with interest only on amounts actually used.

Incentives for First-Time & Small-Scale Investors

Forgivable down payment programs through CHFA can significantly reduce upfront capital requirements. SBA 90% financing provides exceptional leverage for qualified investors. Local grant pools throughout Connecticut offer additional incentives for qualifying projects.

Costs, Rates & Timelines You Can Expect

Understanding the real costs of Connecticut property investment loans is crucial for making smart investment decisions.

DSCR loan rates currently sit between 7.0% and 10.5%. If your property has a strong DSCR ratio above 1.25 and you're putting down 25%, you'll land closer to that 7.0% range.

Conventional investment loan rates range from 5.8% to 8.9%, typically running about 0.625% higher than primary residence rates. Your credit score makes a huge difference - jumping from 680 to 740 can save you nearly half a percentage point.

Hard money rates of 8.9% to 10.9% plus 2-5 origination points start looking reasonable when you can close in 48 hours and secure time-sensitive deals.

Closing timelines vary dramatically. BrightBridge Realty Capital's direct lending model allows DSCR loans to close in 10-14 days, while conventional loans through banks typically take 30-45 days. Hard money loans can close in 48 hours when prepared.

Interest-only versus amortizing payments significantly impacts monthly cash flow. Interest-only loans preserve capital during fix-and-flip projects but need exit strategies. Fully amortizing loans cost more monthly but provide 30-year payment stability.

Points and fees deserve careful attention. Conventional loans might charge 1-2% in origination fees, while hard money lenders often charge 3-5 points. Recent research shows that paying points upfront can make sense for long-term holds.

Escrow requirements add roughly $200-400 monthly but provide budget predictability. Budget for total costs including points, fees, and monthly payments when analyzing deals.

Avoiding Pitfalls & Choosing the Right Lending Partner

Real estate investing in Connecticut can be incredibly rewarding, but it's easy to make costly mistakes that wipe out profits. Here are the most common pitfalls with Connecticut property investment loans.

Under-budgeting renovation costs kills fix-and-flip deals. Always add 20-30% to your contractor's estimate. Ignoring DSCR requirements trips up investors who fall in love with properties before running cash flow numbers. Over-leveraging leaves you vulnerable when vacancy periods or major repairs hit.

Missing documentation is the number one reason deals fall apart at closing. Misreading timelines creates unnecessary stress - know your loan type's realistic timeline and communicate it clearly.

Successful investors shop multiple lenders but don't just focus on rates. A lender offering 7.5% who can close in 10 days might save more money than one offering 7.0% who takes 45 days.

Verify all fees upfront because surprise costs at closing destroy profitability. Use local appraisers who understand Connecticut's unique markets. Align your loan terms with your exit strategy from day one.

Choosing the right lending partner goes beyond finding the lowest rate. You want someone who communicates clearly, understands your market, and has experience with your property type.

At BrightBridge Realty Capital, our direct lending model means you're working directly with decision-makers. Local market knowledge makes a huge difference in Connecticut's diverse real estate landscape.

For more insights on avoiding common lending mistakes, check out our guide on DSCR loans to understand how cash-flow based lending can simplify your investment strategy.

Frequently Asked Questions about Connecticut Property Investment Loans

I get these questions almost daily from investors exploring Connecticut property investment loans. Let me share the real answers based on what I see in the trenches every day.

How much down payment do I really need?

The honest answer? It's not just about the minimum down payment – it's about having enough cash to actually succeed. Conventional loans require 20-25% down and DSCR loans typically ask for 20%, but that's just the starting point.

Here's what I tell my clients: budget 30-35% of the purchase price for your total upfront investment. That covers your down payment, closing costs (usually 2-3% of the loan amount), inspections, appraisals, and those inevitable immediate repairs that pop up.

Hard money loans might only require 10-15% down, which sounds great until you realize you're paying higher rates and points. Sometimes that trade-off makes perfect sense for a quick flip, but don't let the low down payment fool you into thinking it's "cheap" money.

The real game-changer? If you're a veteran, VA loans let you buy up to a four-unit property with zero down payment – as long as you live in one unit. I've helped several veteran investors launch their portfolios this way, and it's honestly one of the best deals in real estate financing.

Can projected rental income help me qualify?

Absolutely, and this is where Connecticut property investment loans get really interesting. Most conventional lenders will count 75% of your projected rental income toward qualification. That's a huge boost to your borrowing power.

For DSCR loans, it gets even better – we qualify you based entirely on the property's rental income potential. No W-2s, no tax returns, no digging through your personal finances. If the property generates enough rent to cover the mortgage payment (we call this a DSCR of 1.0 or higher), you're good to go.

The key is solid documentation. For existing rentals, bring current lease agreements and rent rolls. For new purchases, we'll use market rent analysis or get the appraiser's opinion on rental potential. I've even accepted rental projections from experienced property management companies who know the local market inside and out.

This rental income treatment is honestly for investors. I've helped self-employed borrowers and business owners who couldn't qualify for traditional loans easily get approved through DSCR programs because their properties cash flow beautifully.

How fast can I close on an investment loan in Connecticut?

Speed depends on two things: the loan type you choose and how prepared you are. At BrightBridge Realty Capital, our fastest closing was 48 hours on a hard money deal where the borrower had everything ready to go.

Hard money loans consistently close fastest – usually within 2-5 days when everyone's motivated. DSCR loans typically take 30-45 days, which beats conventional loans that usually run 45-60 days due to all the personal income verification requirements.

But here's the secret sauce: preparation beats everything. The investors who close fastest have their documentation organized before they start shopping, maintain current pre-approval letters, and work with experienced teams who understand investment transactions.

I always tell clients to get pre-approved with multiple loan types before making offers. Having a hard money pre-approval for quick closings and a DSCR pre-approval for better long-term rates gives you flexibility to match your financing to each deal's timeline requirements.

The bottom line? If you need to close fast, we can make it happen. If you have time for the best rates and terms, we'll optimize for that instead. It's all about matching the right tool to your specific situation.

Conclusion & Next Steps

Your journey into Connecticut property investment loans doesn't have to be overwhelming. The Constitution State offers a sweet spot that many investors overlook - stable rental markets without the sky-high prices of neighboring Massachusetts and New York.

At BrightBridge Realty Capital, we've built our reputation on doing what others say can't be done. Need to close in 48 hours? We've done it. Want to finance based purely on cash flow without showing W-2s? Our DSCR loans make it happen. Looking to scale quickly with portfolio financing? We structure deals that banks won't touch.

Our direct lending model cuts out the middleman headaches that slow down traditional banks. When you work with us, you're talking directly to decision-makers who understand real estate investing.

Getting started is simpler than you think. First, get clear on your investment strategy. Next, calculate your real buying power including down payments, closing costs, and renovation reserves. Most successful investors budget about 30-35% of purchase price for total upfront costs.

Pre-approval gives you serious buyer credibility in Connecticut's competitive markets. We provide preliminary approval within 24 hours, giving you the confidence to make strong offers.

The Connecticut market outlook remains bright for prepared investors. College towns maintain steady rental demand regardless of economic cycles. Cities like New Haven, Hartford, and Stamford continue attracting young professionals who prefer renting to buying.

One of our veteran clients used VA financing to acquire a four-unit building in New Haven with zero down payment. Living in one unit while collecting rent from the other three generates $2,400 monthly cash flow. Another client leveraged our DSCR program to acquire three rental properties in six months, building a portfolio that now generates over $5,000 monthly passive income.

Your next step is simple - let's talk about your specific situation and goals. Every investor's path looks different, and cookie-cutter solutions rarely work. We'll help you steer Connecticut's loan landscape and structure financing that actually makes sense for your strategy.

Ready to turn your Connecticut investment vision into reality? Our experienced team understands both the opportunities and challenges of investing in the Constitution State.

More info about custom funding solutions | More info about DSCR loans

The Connecticut real estate market rewards investors who move quickly with proper financing in place. Let's make sure you're ready to act when the right deal comes along.