Multifamily Property Loans Explained: Investing in Your Future

Summary

Discover multifamily investment property loans, compare options, and learn how to finance your next real estate investment today.

Why Multifamily Investment Property Loans Are Essential for Smart Real Estate Investors

Multifamily investment property loans are specialized financing products designed for properties with five or more residential units, offering investors a pathway to scale their portfolios while generating consistent cash flow. These loans differ significantly from traditional residential mortgages in their underwriting approach, focusing on the property's income-generating potential rather than just personal income.

Quick Overview: Multifamily Investment Property Loans

- Property Types: 5+ unit apartment buildings, complexes, and mixed-use properties

- Loan Amounts: Typically $1M to $75M+ (varies by lender and program)

- Down Payment: 20-35% depending on loan type and property condition

- Key Metrics: Debt Service Coverage Ratio (DSCR) of 1.20x-1.40x minimum

- Common Terms: 5-30 years with various amortization schedules

- Top Options: Agency loans (Fannie Mae/Freddie Mac), FHA/HUD programs, bridge loans, CMBS

The multifamily sector has proven remarkably resilient, with average national asking rents reaching $1,729 in 2024 and vacancy rates holding steady at 8.0%. This stability makes multifamily properties attractive for investors seeking predictable returns and portfolio diversification.

Unlike single-family rentals where one vacancy can eliminate 100% of income, multifamily properties spread risk across multiple units. When structured properly, these investments can provide steady cash flow while building long-term wealth through appreciation and debt paydown.

The financing landscape offers multiple paths forward - from Fannie Mae's conventional products with up to 80% leverage to FHA-insured loans reaching 85-90% loan-to-value ratios. Bridge loans provide quick access to capital for value-add opportunities, while agency programs offer long-term stability with competitive rates.

I'm Daniel Lopez, a loan officer at BrightBridge Realty Capital with extensive experience structuring multifamily investment property loans for investors seeking flexible, fast-closing solutions. My focus is helping investors steer the complex world of multifamily financing to maximize their investment potential.

Multifamily investment property loans word guide:- multifamily bridge loan lender- fast capital for real estate- direct real estate lending

Understanding Multifamily Investment Property Loans

Multifamily investment property loans are the bridge between residential mortgages and full commercial financing. These specialized loans are designed for residential properties with five or more dwelling units - and that magic number of five makes all the difference in how lenders view your investment.

A duplex or fourplex still falls under residential mortgage guidelines, but add just one more unit and suddenly you're in commercial lending territory. This shift in perspective actually works in your favor.

Government-sponsored enterprises like Fannie Mae and Freddie Mac recognize that larger multifamily properties operate more like businesses than homes. The Loan We All Own through Fannie Mae has financed over 10 million multifamily units over the past 35 years. More than 90% of these apartments serve workforce housing - properties affordable to families earning at or below 120% of area median income.

Portfolio lenders offer another compelling path forward. These banks and credit unions hold loans on their books rather than selling them off, which means they can bend the rules when it makes sense. They're not locked into rigid agency guidelines, though you'll typically see shorter terms.

The liquidity aspect is crucial too. Unlike single-family properties where finding buyers can take months, well-performing multifamily properties attract serious investor interest quickly.

Why Invest in Multifamily Real Estate

The numbers tell a compelling story about rental demand in today's market. With homeownership rates sitting near historic lows, there's a massive pool of potential tenants who either can't or won't buy homes.

During economic uncertainty, many families postpone homebuying decisions, which actually strengthens rental demand. Recession resilience is where multifamily properties really shine. While luxury developments might struggle during downturns, workforce housing maintains steady occupancy.

The scalability factor is a game-changer for serious investors. Instead of juggling maintenance calls from properties scattered across different counties, you can concentrate units in one location, dramatically reducing management costs.

How These Loans Differ from Single-Family & Commercial Mortgages

Multifamily investment property loans occupy fascinating middle ground between residential and commercial financing. The underwriting focus shifts dramatically from your personal financial picture to the property's income-generating ability.

While single-family investment loans heavily weight your W-2 income and credit score, multifamily lenders care most about one thing: can this property income cover the mortgage payments with room to spare? The Debt Service Coverage Ratio (DSCR) becomes your new best friend - typically requiring net operating income to exceed debt service by 20-40%.

Amortization schedules get more creative in the multifamily world. Residential loans love their 30-year fully amortizing terms, but commercial multifamily loans often use shorter amortization periods with balloon payments. However, agency programs can still offer that comfortable 30-year amortization.

Term length flexibility is where multifamily financing really shines. Bridge loans might run just 18-24 months for value-add projects, while HUD programs can extend beyond 40 years for new construction.

Multifamily Loan Types & Side-by-Side Comparison

Choosing the right financing for your multifamily property can feel overwhelming with so many options available. Each loan type serves a specific purpose and investment strategy.

Conventional bank loans offer the simplest path forward, typically requiring 20-25% down payments with competitive rates. The catch? You'll likely need to provide a personal guarantee, and the leverage might not be as attractive as other options.

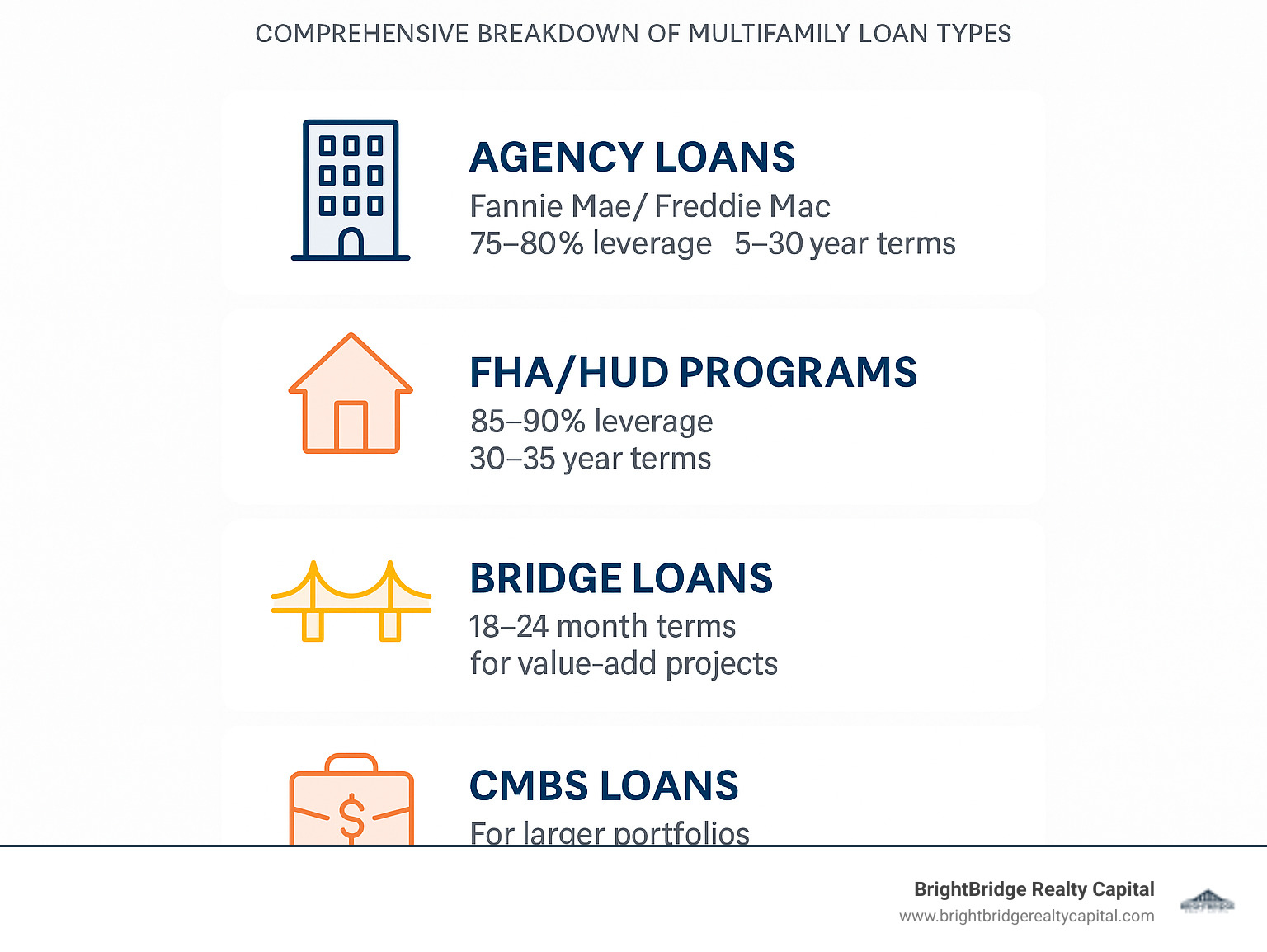

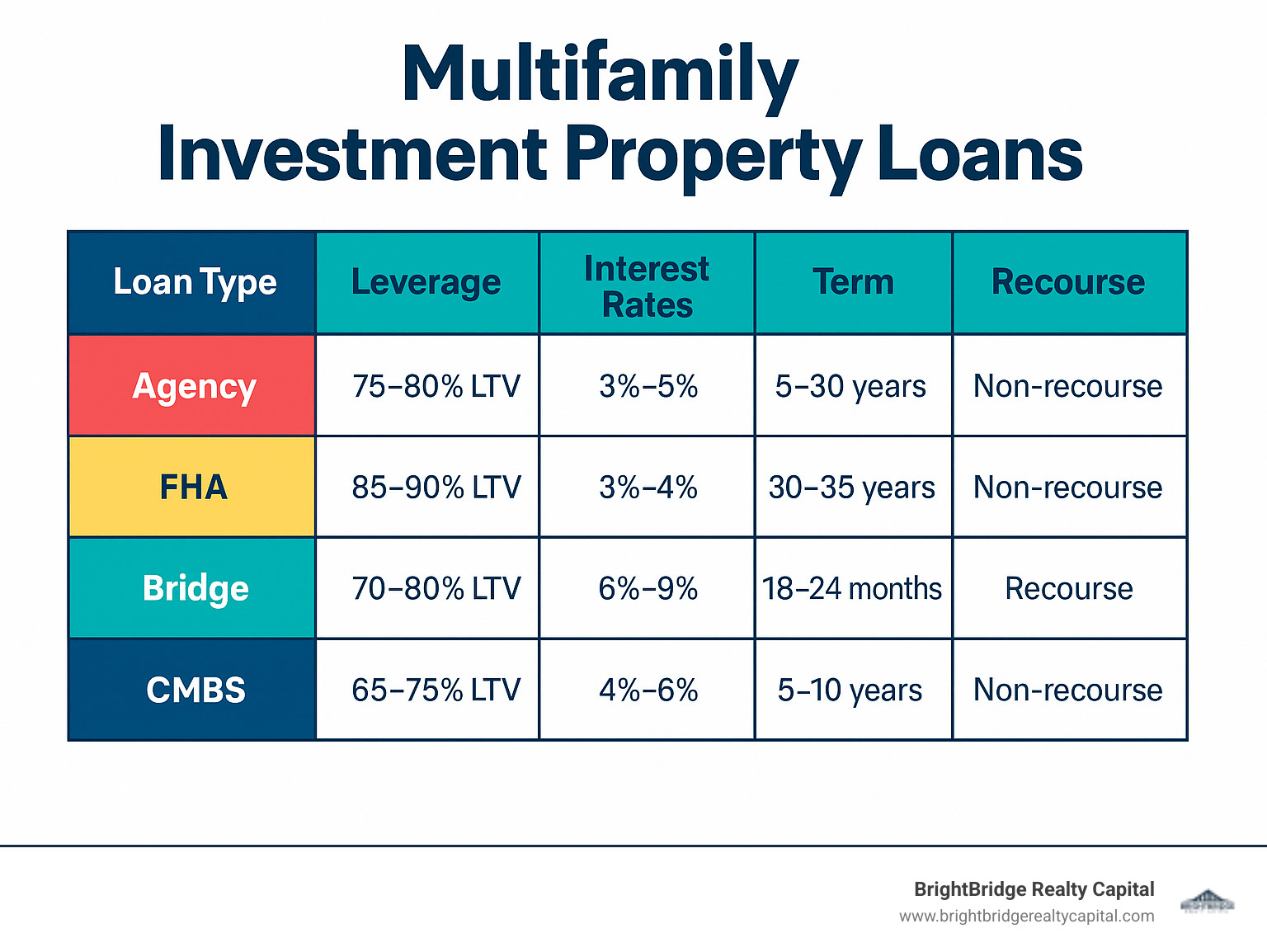

Agency loans through Fannie Mae and Freddie Mac represent the gold standard of multifamily investment property loans. With 75-80% leverage, competitive rates, and non-recourse terms for loans over $750,000, it's easy to see why they dominate the market.

For maximum leverage, FHA and HUD programs can't be beat, offering up to 85-90% loan-to-value ratios with fully amortizing terms stretching 30-35 years. The trade-off? Expect longer approval timelines of 6-12 months and stricter compliance requirements.

CMBS loans serve the larger deal market, typically handling transactions from $1 million to $1 billion. These focus more on property quality than borrower strength, making them ideal for institutional-grade assets.

When speed matters most, bridge and hard money solutions provide quick access to capital in 30-60 days. Terms run 18-24 months with higher rates, but the flexibility can make all the difference for time-sensitive opportunities.

Life insurance company loans cater to institutional-quality properties with experienced sponsors. They offer very competitive rates for Grade A assets but require lower leverage and prefer long-term relationships.

Agency-Backed Options

Fannie Mae and Freddie Mac have revolutionized multifamily lending through their Delegated Underwriting and Servicing programs. These government-sponsored enterprises buy loans from approved lenders, creating steady capital flow and standardized terms.

Fannie Mae's conventional products deliver up to 80% loan-to-value ratios with minimum 1.25x debt service coverage requirements. Terms span from 5 to 30 years with various interest rate options. You'll need stabilized occupancy of 90% for 90 days before funding.

Freddie Mac's Small Balance Loans serve the $1 million to $7.5 million market with streamlined processing. The automatic rate locks at letter of intent execution eliminate early rate-lock costs and provide certainty from day one.

Both agencies offer green financing incentives for energy-efficient properties. If your building meets certain environmental standards, you can access reduced pricing and higher leverage.

FHA & HUD Programs

HUD's multifamily programs offer the highest leverage available in the market, making them incredibly attractive for investors who want to maximize their purchasing power.

HUD 221(d)(4) handles new construction and major renovations with terms exceeding 40 years and loan-to-cost ratios reaching 87% or higher. This program works beautifully for ground-up development.

HUD 223(f) serves existing properties with up to 35 years of fully amortizing terms and high leverage ratios. It's perfect for stabilized acquisitions where you want maximum leverage and aren't in a rush to close.

HUD 223(a)(7) offers faster refinancing for existing HUD borrowers. If you already have a HUD loan and want to take advantage of better market conditions, this program lets you skip much of the lengthy initial underwriting process.

Bridge & Hard-Money Solutions

Bridge financing shines when timing is everything. Whether you're competing against cash buyers or found a property that needs work before qualifying for permanent financing, bridge loans provide the speed traditional lenders can't match.

Interest-only payments during the bridge period preserve your cash flow for renovations and operations. Yes, rates are higher than permanent financing, but the speed often justifies the cost. Most bridge lenders can close within 30-60 days compared to 90+ days for agency loans.

Value-add scenarios represent bridge financing's sweet spot. That property with below-market rents, deferred maintenance, or low occupancy? Bridge loans let you acquire it quickly, implement improvements, then refinance into permanent financing at a higher valuation.

Exit strategy planning becomes critical with these short-term loans. Successful investors have clear plans for permanent refinancing or sale before the bridge term expires.

Niche & Private Capital Choices

Life insurance company loans target the absolute best properties with seasoned sponsors. These lenders offer rates that often beat agency pricing, but they require low leverage (60-70% LTV) and institutional-grade assets.

Credit unions sometimes surprise investors with competitive multifamily financing, especially for local properties or members with existing relationships.

DSCR loans focus purely on property cash flow without traditional income verification. These products serve self-employed investors or those with complex tax situations where W-2s don't tell the whole story.

The private capital landscape keeps expanding, giving investors more options than ever. The key is matching your capital source with your specific strategy and timeline.

Qualifying & Underwriting Essentials

Getting approved for multifamily investment property loans feels different than qualifying for a house loan. The property becomes the star of the show, not just your personal income. This shift in focus can actually work in your favor - a well-performing apartment building can carry more weight than your W-2.

The Loan-to-Value (LTV) ratio sets the stage for how much you'll need to bring to the table. Most lenders work within the 70-80% range, though some programs stretch to 85-90% for the right deals. Lenders always use the lower of purchase price or appraised value.

Debt Service Coverage Ratio (DSCR) becomes your new best friend in multifamily lending. This metric shows whether your property makes enough money to comfortably pay its mortgage. Most lenders want to see at least 1.20x to 1.25x coverage, meaning your net operating income exceeds debt payments by 20-25%.

The debt yield calculation provides another lens for lenders to evaluate risk. They divide your property's net operating income by the total loan amount, typically requiring 8-10% minimum.

Your credit score still matters, though it's not the make-or-break factor it is with residential loans. Most programs require scores between 620-680, with higher scores opening doors to better pricing.

Net worth and liquidity requirements ensure you can handle unexpected challenges. Many lenders want to see net worth equal to your loan amount. Liquid assets covering 6-12 months of debt service provide additional comfort.

Minimum Down Payment for Multifamily Investment Property Loans

Down payment requirements create the biggest hurdle for many investors. Conventional bank loans typically ask for 20-25% down, which represents the baseline expectation across most programs.

Agency programs through Fannie Mae and Freddie Mac often accept 20% down payments for experienced borrowers with strong deals. These programs offer some of the best leverage available in the market.

FHA and HUD programs shine for cash-constrained investors, sometimes accepting down payments as low as 10-15%. The trade-off comes in extended approval timelines and comprehensive compliance requirements.

Bridge loans typically require 25-35% down payments, reflecting their higher risk profile and shorter terms. However, many bridge lenders structure payments as interest-only during the loan term.

Reserve requirements add another layer to your cash needs beyond the down payment. Most lenders require 2-6 months of debt service payments held in reserve accounts, plus replacement reserves for future capital improvements.

Recourse vs Non-Recourse in Multifamily Investment Property Loans

The recourse question significantly impacts your personal liability and investment structure. Non-recourse loans limit the lender's recovery to the pledged property itself, protecting your other assets if things go sideways.

Agency loans over $750,000 typically offer non-recourse terms with standard carve-outs for bad acts like fraud, misrepresentation, bankruptcy, and environmental issues. This protection makes agency financing particularly attractive for serious investors.

Bank loans often come with full recourse requirements, meaning you're personally guaranteeing the debt. While this increases your personal risk, banks may offer more competitive pricing in exchange for the additional security.

Carve-out guarantees represent a middle ground between full recourse and non-recourse structures. The loan operates as non-recourse under normal circumstances, but you guarantee specific "bad acts" like environmental violations or fraud.

Entity structuring plays a crucial role in non-recourse lending. Lenders often require single-purpose entities (SPEs) to own the property, providing additional protection for the lender while preserving non-recourse benefits for you.

From Application to Closing: Timeline, Fees & Pitfalls

Getting from application to closing on multifamily investment property loans doesn't have to be overwhelming. The key is understanding what to expect and preparing for each step along the way.

The journey typically starts with a letter of intent (LOI), which is your formal way of saying "let's do this deal." You'll put down an application deposit - usually between $10,000 and $50,000 - which shows you're serious and helps fund the initial work.

Once your LOI is signed, the real work begins. Third-party reports become your new reality. The appraisal alone can take 2-3 weeks, and environmental studies add another layer of complexity. Each report costs money and takes time, but they're essential for protecting both you and your lender.

The timeline varies dramatically based on your loan choice. Bridge loans can close in 30-45 days if everything goes smoothly. Agency loans through Fannie Mae or Freddie Mac typically take 60-90 days, while HUD programs can stretch 6-12 months.

Rate locks become crucial during volatile market periods. Most lenders offer 30-180 day protection, and some programs like Freddie Mac's Small Balance Loans automatically lock your rate when you sign the LOI.

Legal review ties everything together, but it's also where things can go sideways. Title issues found late in the process can derail deals, so using experienced multifamily attorneys isn't just smart - it's essential.

For investors considering development projects, ground-up construction loans require even more specialized expertise and longer timelines due to their construction-to-permanent financing structures.

Step-by-Step Process

Smart investors start gathering documents before they even submit their LOI. Your document checklist should include 2-3 years of property financials, current rent rolls, your personal financial statements, tax returns, and entity formation documents.

The application deposit does double duty - it shows you're committed and funds the initial underwriting work. Most deposits get applied to your closing costs, but walk away without good reason and you might lose it.

During underwriting review, expect questions. Underwriters examine every detail of both your property and your qualifications. The faster you respond, the faster you close.

Loan commitment is your finish line - almost. You'll receive final approval with specific conditions that must be met before closing. Common requirements include updated insurance certificates, final rent rolls, and resolution of any title issues.

Closing coordination involves more moving parts than you might expect. Pre-closing calls help catch problems before they become deal-killers.

Typical Costs & How to Reduce Them

Closing costs on multifamily investment property loans can add up quickly. Origination fees typically run 0.5-2.0% of your loan amount. Agency loans often charge less than bridge or hard money options.

Third-party costs are largely unavoidable but manageable. Appraisals run $5,000-15,000 depending on property size. Environmental reports add $3,000-8,000, property condition assessments cost another $3,000-8,000, and legal fees can range from $5,000-25,000.

Rate lock deposits might be required if you need extended protection or rates are particularly volatile. Expect to pay 0.25-1.0% for longer locks, though most lenders apply these fees to your closing costs.

Prepayment penalties deserve special attention because they affect your future flexibility. Agency loans typically use yield maintenance calculations - complex formulas that can result in substantial penalties if rates have dropped since you closed.

The best way to reduce costs? Work with experienced professionals who know the multifamily space inside and out. Complete documentation packages prevent delays, and selecting the right loan product for your situation avoids unnecessary complications.

At BrightBridge Realty Capital, we've streamlined this entire process to deliver closings in as little as one week. Our direct lending approach eliminates intermediaries and reduces both costs and delays.

Conclusion

The world of multifamily investment property loans might seem complex at first glance, but it's really about matching the right financing tool to your investment goals. Think of it like choosing the right wrench for a specific bolt - each loan type serves a purpose, and understanding these differences can transform your investment results.

Whether you're eyeing your first 12-unit building or adding another property to an existing portfolio, the financing landscape offers genuine opportunities. Agency loans provide the stability many investors crave with their long terms and competitive rates. Bridge financing opens doors to value-add deals that might otherwise slip away. And HUD programs can stretch your down payment further than you might think possible.

The key insight I've learned after years in this business is simple: the right financing structure often matters more than finding the perfect property. A mediocre building with great financing can outperform an excellent property saddled with poor loan terms. It's that straightforward.

At BrightBridge Realty Capital, we've built our reputation on understanding this principle. Our direct lending approach means you're working with decision-makers, not intermediaries who slow things down. When we say we can close within a week, we mean it - because sometimes the best deals don't wait around for lengthy approval processes.

The multifamily market's fundamentals remain rock-solid. People need places to live regardless of economic headlines. Rental demand stays consistent even when other investment sectors get shaky. This stability, combined with the cash flow potential and tax advantages, explains why experienced investors keep coming back to multifamily properties.

Your next step depends on where you are in your investment journey. Maybe you're ready to move beyond single-family rentals and want the operational efficiency that comes with having all your units in one location. Or perhaps you're looking to refinance existing properties to pull out equity for the next acquisition.

Whatever your situation, multifamily investment property loans offer pathways to build lasting wealth through real estate. The variety of options means there's likely a financing solution that fits your specific needs and timeline.

Ready to explore what's possible for your multifamily investment goals? Take a look at our comprehensive financing solutions at More info about financing solutions and see how our streamlined approach can help you move quickly on opportunities in today's competitive market.