Unlocking Commercial Real Estate with No Doc Loans

Summary

Unlock real estate with commercial no doc loans. Get fast funding, streamline applications, and bypass traditional income verification.

Why Commercial No-Doc Loans Are Changing Real Estate Investment

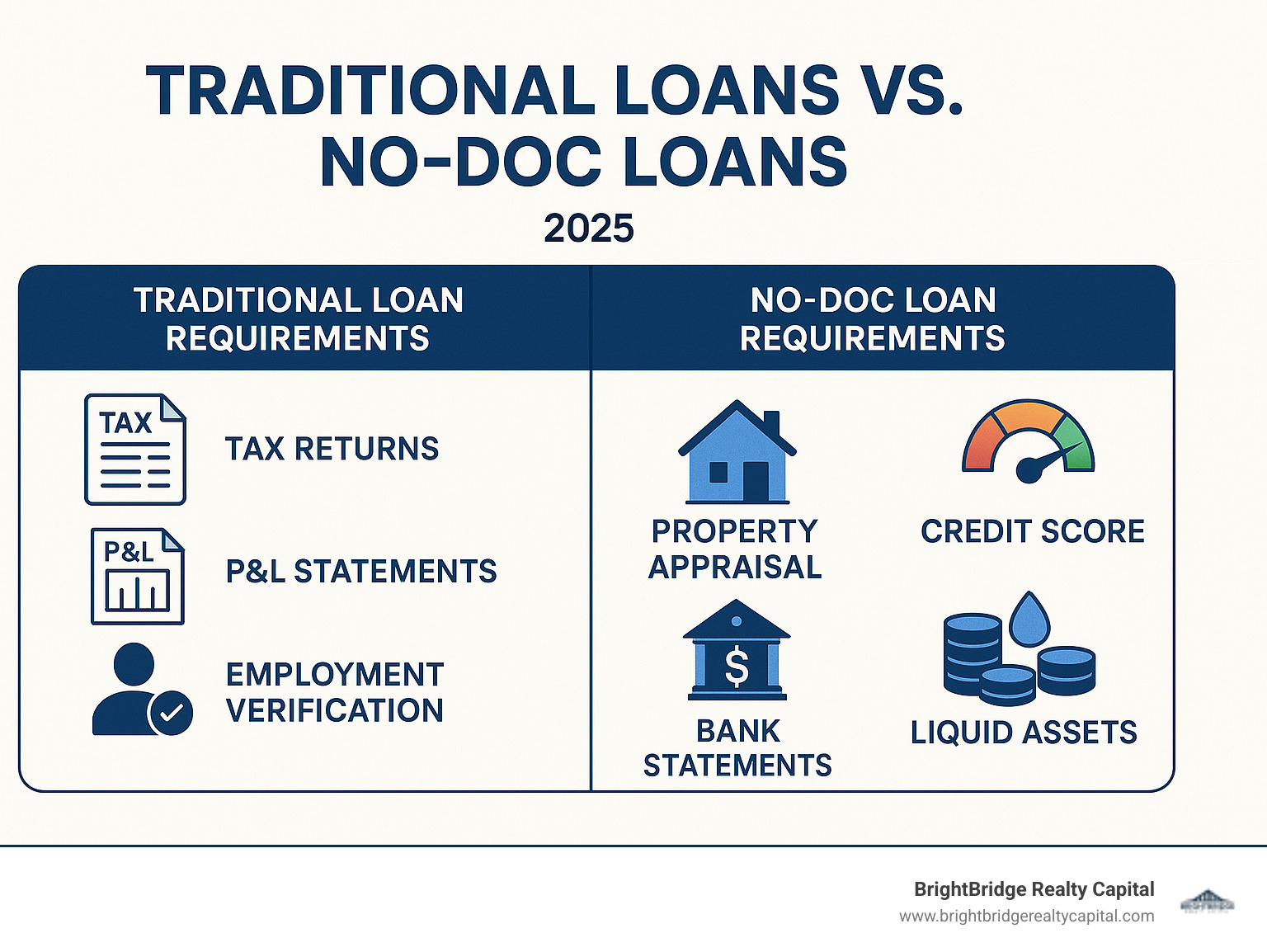

Commercial no-doc loans let qualified real-estate investors bypass the mountain of tax returns and P&Ls banks usually demand. Lenders underwrite mainly on the property's value and your credit profile, so you can move fast when a deal pops up.

Quick facts

- What they are: asset-based commercial loans with limited income docs

- Loan amounts: $100,000 – $5 million+

- Rates: roughly 5.88% – 8.49%

- Closing time: as little as 7 business days

- Down payment: normally 25-30%

- Minimum credit: 650 FICO

Traditional bank approvals can drag on for 60-90 days—long enough for another buyer to steal the deal. BrightBridge Realty Capital's no-doc program flips the script by focusing on collateral, credit, and reserves. You trade a slightly higher rate and bigger down payment for speed, privacy, and a process that rarely tops twenty pages of paperwork.

I'm Daniel Lopez, a loan officer at BrightBridge Realty Capital. I've watched investors win multifamily, retail, and mixed-use assets because they could close in a week.

Must-know commercial no-doc terms:

Understanding Commercial No-Doc Loans: A Shift from Traditional Financing

While banks require extensive documentation, private lenders take a different approach. Instead of analyzing every line of your tax return, a no-doc lender asks two main questions: "Is the property a solid asset?" and "Does the borrower have good credit and cash reserves?" This mindset is the core of modern asset-based lending.

What Is a Commercial No-Doc Loan?

A commercial no-doc loan bypasses traditional income verification. You'll provide a credit report, bank statements, and an appraisal, but not years of corporate tax returns. Because the loan is non-QM (not a Qualified Mortgage), the lender focuses on metrics like loan-to-value (LTV) and the property's cash flow.

This financing model evolved to serve successful real estate investors who often structure their businesses for tax efficiency, showing minimal taxable income despite having substantial cash flow. Commercial no-doc loans operate under different rules than residential mortgages, as the Dodd-Frank Act's QM rules don't apply to most commercial deals. This gives lenders the flexibility to prioritize asset quality over documented income, filling a gap that traditional banking often ignores.

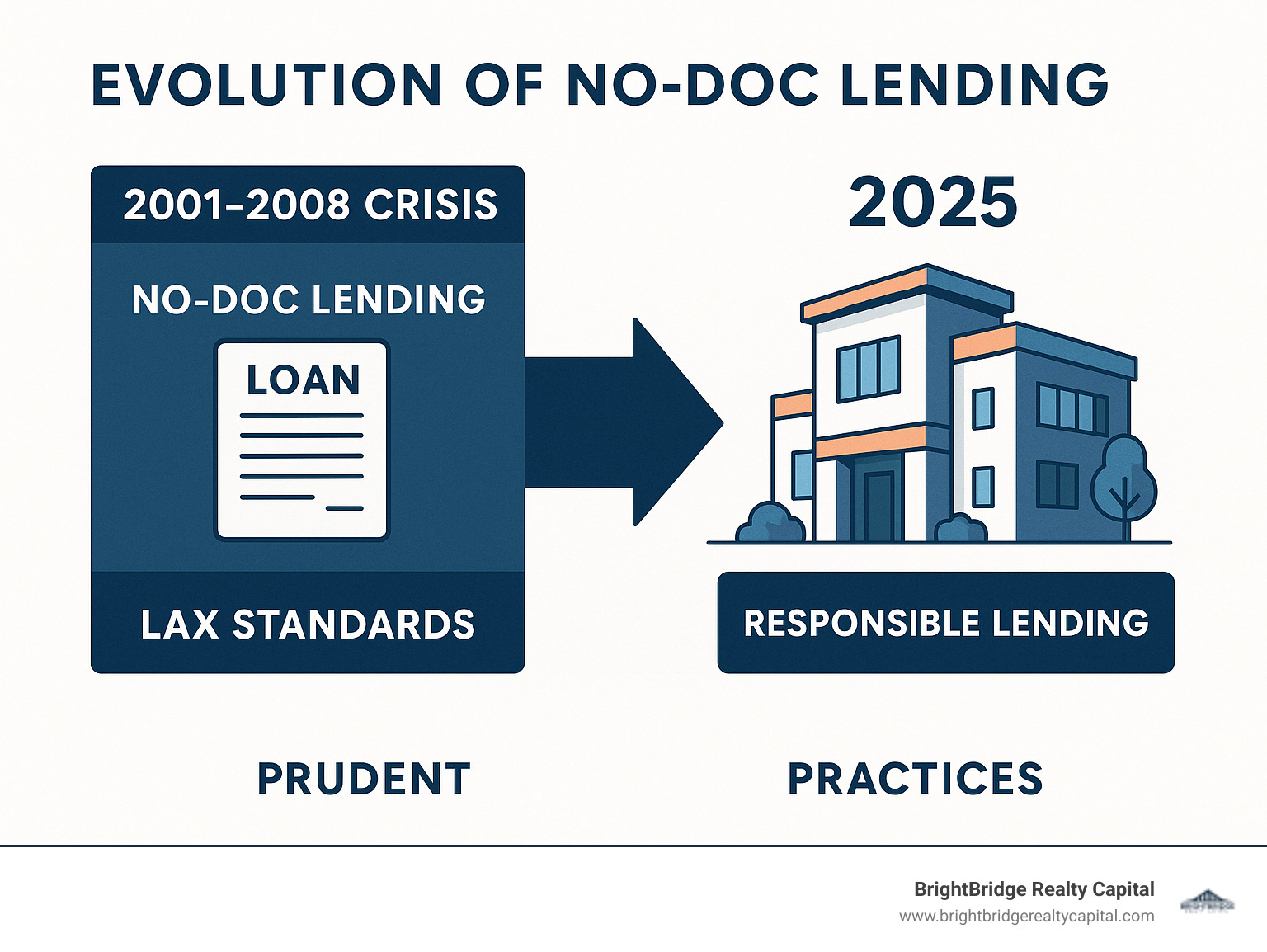

The rise of no-doc commercial lending can be traced back to the post-2008 financial crisis era, when traditional banks tightened their lending standards significantly. While this created safer lending practices, it also left many qualified investors without access to capital. Private lenders stepped in to fill this void, developing sophisticated underwriting models that could assess risk without relying heavily on tax returns and profit-and-loss statements.

Today's no-doc lenders use advanced property valuation techniques, including automated valuation models (AVMs), comparative market analysis, and detailed cash flow projections. They also leverage technology to quickly verify assets, analyze bank statements, and assess creditworthiness. This technological advancement has made the underwriting process both faster and more accurate than traditional methods in many cases.

How No-Doc Loans Differ from Traditional Bank Loans

| Traditional Bank | Commercial No-Doc | |

|---|---|---|

| Paperwork | 2-3 yrs tax returns, P&Ls, rent rolls | Credit, appraisal, bank statements |

| Time to close | 45-90 days | 7-14 business days |

| Max LTV | ~80% | 70-75% |

| Rates | Lower | 1-3% higher |

| Flexibility | Rigid terms | Interest-only, balloons, hybrids |

The core differences highlighted in the table stem from a fundamental shift in underwriting philosophy. Traditional banks see the borrower's income as the primary source of repayment. They require extensive paperwork, follow rigid procedures, and involve slow-moving loan committees, creating delays that can jeopardize time-sensitive deals.

No-doc lenders flip this model. They treat the property's income potential and the borrower's equity as the primary repayment factors. This streamlined approach focuses on creditworthiness, asset verification, and property value. It allows for faster decisions, often made by empowered underwriters, and more flexible loan structures like interest-only periods or hybrid rates.

The regulatory environment also plays a crucial role in these differences. Traditional banks operate under strict federal regulations that require extensive documentation and standardized underwriting procedures. These regulations, while designed to protect consumers and ensure financial stability, can create bureaucratic bottlenecks that slow down the lending process.

Private no-doc lenders, while still regulated, operate under different rules that allow for more flexibility in their underwriting approach. They can make decisions based on the specific merits of each deal rather than adhering to rigid guidelines that may not account for the unique circumstances of sophisticated real estate investors.

For investors who are self-employed, have complex income streams, or simply value speed and privacy, the no-doc route removes major obstacles. While the rates are higher, many consider it a worthwhile trade-off to secure properties before the competition. The ability to close quickly can often mean the difference between securing a profitable deal and losing it to a competitor with faster financing.

The flexibility in loan structures is another significant advantage. Traditional banks typically offer standardized loan products with limited customization options. No-doc lenders can structure loans with interest-only periods during renovation phases, balloon payments that align with exit strategies, or hybrid adjustable rates that start fixed and then adjust based on market conditions.

Want to brush up on the basics? Check out corporate finance essentials.

Who Benefits and What Properties Qualify?

- FICO 650+ (700+ preferred)

- 25-30% cash down plus 6-12 months of reserves

- Verifiable liquid assets

- Some real-estate experience (helps but isn't mandatory)

- No recent bankruptcies or foreclosures

Self-employed professionals, fix-and-flip operators, foreign nationals, and entrepreneurs with complex or irregular income often fit this profile. They let the property's numbers do the talking instead of navigating complex income verification.

Ideal Borrower Profiles

No-doc loans are a great fit for:

Self-employed professionals & business owners: Their tax returns may not reflect their true cash flow due to legitimate business deductions. Many successful entrepreneurs write off significant expenses, depreciate assets, and structure their businesses in ways that minimize taxable income while maximizing actual cash flow. A restaurant owner, for example, might show minimal profit on paper after accounting for equipment depreciation, but have substantial monthly cash flow. Similarly, real estate professionals often have complex income streams from commissions, property management fees, and investment returns that don't translate well to traditional income documentation.

Real estate investors: Those with multiple properties, complex LLC structures, or depreciation write-offs can avoid documentation headaches. Experienced investors often own properties through various legal entities for liability protection and tax optimization. They might have a portfolio of rental properties generating strong cash flow, but their personal tax returns show losses due to depreciation deductions. Traditional lenders struggle to underwrite these complex structures, while no-doc lenders focus on the underlying asset quality and the investor's track record.

Foreign nationals: Investors who lack U.S. credit history or tax returns but have substantial assets can qualify. International investors bring significant capital to U.S. real estate markets but often face barriers with traditional financing due to lack of domestic credit history or unfamiliar income documentation from their home countries. No-doc lenders can work with foreign bank statements, asset verification from international institutions, and focus on the property's fundamentals rather than complex cross-border income verification.

High-net-worth individuals: Borrowers who prioritize speed and financial privacy over securing the lowest possible rate. Wealthy individuals often have diverse investment portfolios, trust structures, and complex financial arrangements that make traditional income verification cumbersome. They may prefer to keep their financial details private and are willing to pay higher rates for the convenience and discretion that no-doc loans provide.

Business owners in transition: Those with irregular income due to a company sale or retirement can use assets to qualify. Entrepreneurs who have recently sold businesses, professionals transitioning between careers, or retirees with substantial assets but limited current income can benefit from asset-based underwriting. Their financial strength lies in their accumulated wealth rather than current income streams.

Fix-and-flip investors: These investors need speed to capitalize on opportunities and often have irregular income patterns based on project completions. Traditional lenders struggle with the cyclical nature of flip income, but no-doc lenders can focus on the investor's experience, the property's potential, and the exit strategy.

Eligible Commercial Property Types

No-doc capital works best on standard, cash-flowing properties in healthy markets:

Multifamily buildings (5+ units): These properties are favored by lenders due to their predictable income streams and strong demand fundamentals. Apartment buildings with established rent rolls, good occupancy rates, and stable tenant bases are ideal candidates. Lenders appreciate the diversified income from multiple units, which reduces the risk of total income loss. Properties in growing metropolitan areas with strong job markets and population growth are particularly attractive.

Mixed-use assets (residential over retail): These properties combine the stability of residential income with the potential upside of commercial rents. Ground-floor retail with apartments above is a common configuration that appeals to no-doc lenders. The residential component provides steady cash flow while the retail space can offer higher per-square-foot rents. Location is crucial for these properties, with urban and suburban main street locations being preferred.

Stabilized retail or strip centers: Shopping centers with established tenant bases and long-term leases are good candidates for no-doc financing. Lenders look for properties with creditworthy tenants, diverse tenant mixes to avoid over-reliance on any single business, and locations in areas with strong demographics. Properties anchored by national chains or essential services like grocery stores, pharmacies, or medical offices are particularly attractive.

Office or medical buildings with seasoned tenants: Professional office buildings and medical facilities with established tenant relationships and long-term leases work well for no-doc financing. Medical properties are especially favored due to the specialized nature of the improvements and the tendency for medical tenants to stay long-term. Office buildings in suburban markets with ample parking and good access are preferred over urban high-rises.

Warehouses and light industrial: The growth of e-commerce has increased demand for industrial properties, making them attractive to no-doc lenders. Distribution centers, manufacturing facilities, and flex spaces in strategic locations near transportation hubs are particularly sought after. These properties often have long-term leases with creditworthy tenants and require minimal ongoing management.

Self-storage facilities: These properties have gained popularity due to their recession-resistant income streams and relatively low management requirements. Modern self-storage facilities with good locations, security systems, and professional management are attractive to lenders. The month-to-month rental structure allows for quick rent adjustments, and the diverse customer base reduces risk.

Lenders favor properties with predictable income streams and avoid those requiring significant capital improvements or located in declining markets. Properties with environmental issues, deferred maintenance, or challenging tenant situations are typically excluded from no-doc programs. The key is demonstrating stable cash flow and a clear path to loan repayment through property income or exit strategy execution.

The Nuts and Bolts: Types, Terms, and Requirements for Commercial No-Doc Loans

Common No-Doc & Low-Doc Structures

| Loan Type | Docs Needed | Typical Use |

|---|---|---|

| SIVA (Stated-Income, Verified-Assets) | 2-3 months bank statements, appraisal, credit | Self-employed buyers |

| NIVA (No-Income, Verified-Assets) | Asset statements, appraisal, credit | High-net-worth borrowers |

| Bank-Statement Loan | 12-24 mo. business statements | Owners with strong cash flow |

| Asset-Based / Hard Money | Appraisal + down payment | Fix-and-flip or bridge |

SIVA (Stated-Income, Verified-Assets) loans are common for self-employed borrowers. You state your income and verify it with bank statements showing consistent deposits, rather than providing tax returns.

NIVA (No-Income, Verified-Assets) loans disregard income entirely, focusing on the borrower's liquid assets and the property's value. This suits retirees or high-net-worth individuals with substantial assets but low reported income.

Bank-Statement Loans are for business owners with strong cash flow. Lenders analyze 12-24 months of business bank statements to determine a qualifying income based on average monthly deposits.

Asset-Based/Hard Money loans are short-term loans focused almost exclusively on the property's value (or after-repair value). With higher rates and faster closings, they are ideal for fix-and-flip or bridge financing scenarios.

Typical Deal Metrics

- Amounts: $100k to $5M+

- Interest: about 5.9%-8.5% (fixed or hybrid ARM)

- Max LTV: 75% (often 65% for specialty assets)

- Terms: 12-36-month interest-only bridge or 5/1, 30-year amortizing permanent

- Origination: 0.5%-2%

These metrics vary based on the deal's specifics. Interest rates are typically 1-3% higher than bank loans to account for the added risk. Loan-to-Value (LTV) ratios are more conservative, usually capping at 70-75% to ensure the borrower has significant equity in the property. Loan terms can be structured as short-term interest-only bridge loans or longer-term amortizing loans to fit the investor's strategy.

Core Eligibility Checklist

- Minimum 650 credit score

- 25-30% equity at close

- Third-party appraisal supporting value

- Proof of liquidity for down payment plus reserves

- Evidence of insurance and clean title

To qualify, lenders focus on these core elements. A credit score of 650 is the typical minimum, with better terms for scores over 700. A significant down payment (equity) of 25-30% is crucial as it's the lender's primary risk protection. A third-party appraisal must validate the property's value. Borrowers must also show they have sufficient liquid assets for the down payment and 6-12 months of payment reserves. Finally, standard insurance and a clean title are required to protect both parties.

BrightBridge can usually issue a term sheet within 24 hours and fund once the appraisal and title work are back—often in under a week. This rapid turnaround time represents a significant competitive advantage in fast-moving real estate markets where delays can cost deals.

The Strategic Trade-Off: Advantages vs. Disadvantages

Why Investors Choose No-Doc

Close in 7-14 days—compete with cash buyers: In competitive real estate markets, speed often determines who wins the deal. Traditional bank financing can take 45-90 days, during which sellers may accept other offers or market conditions may change. No-doc loans allow investors to present offers with financing contingencies that are nearly as attractive as cash offers. This speed advantage is particularly valuable in hot markets where multiple buyers are competing for the same property.

The ability to close quickly also provides negotiating leverage. Sellers often accept slightly lower offers from buyers who can close fast and with certainty. This speed premium can offset some of the higher costs associated with no-doc financing. Additionally, quick closings reduce the risk of deals falling through due to changing market conditions, interest rate fluctuations, or competing offers.

20 pages of paperwork instead of 200: Traditional commercial loans require extensive documentation including multiple years of tax returns, profit and loss statements, rent rolls, operating statements, personal financial statements, and detailed business plans. The documentation process alone can take weeks to compile and often requires accountant involvement.

No-doc loans streamline this process dramatically. The typical application package includes a loan application, personal financial statement, bank statements, credit authorization, and property information. This reduced paperwork burden saves time and reduces the administrative costs associated with loan applications. It also means fewer opportunities for documentation issues to derail the loan process.

Perfect for unconventional income or multiple LLCs: Many successful real estate investors structure their businesses in ways that optimize tax efficiency but complicate traditional underwriting. They might own properties through various LLCs, have income from multiple sources, or show paper losses due to depreciation while maintaining strong cash flow.

Traditional lenders struggle to underwrite these complex structures and often require extensive explanations, additional documentation, and lengthy review processes. No-doc lenders focus on the borrower's overall financial strength and the property's fundamentals rather than trying to parse complex business structures.

Keep tax returns and business books private: Financial privacy is increasingly important to high-net-worth individuals and successful business owners. Traditional lending requires sharing detailed financial information with multiple parties including loan officers, underwriters, and loan committee members.

No-doc loans provide a level of financial privacy that many borrowers value. While lenders still verify assets and creditworthiness, they don't require detailed income documentation that reveals business strategies, profit margins, or personal financial details.

Lenders can tailor structures—interest-only, flexible pre-pay, hybrids: Traditional banks offer standardized loan products with limited customization options. No-doc lenders can structure loans to match specific investment strategies and cash flow needs.

Interest-only periods are common during renovation phases or lease-up periods when cash flow might be limited. Flexible prepayment terms allow investors to refinance or sell without significant penalties. Hybrid adjustable-rate mortgages can provide initial rate stability with the potential for rate adjustments based on market conditions.

What You Give Up

Rates roughly 100-300 basis points higher than bank debt: The convenience and speed of no-doc loans come at a cost. Interest rates are typically 1-3% higher than traditional bank financing. On a $1 million loan, this translates to $10,000-$30,000 in additional annual interest expense.

This rate premium reflects the additional risk that lenders perceive when underwriting without full income documentation. However, the rate differential has narrowed in recent years as no-doc lenders have refined their underwriting processes and built track records of successful loans.

Investors must carefully analyze whether the benefits of speed and convenience justify the additional cost. In many cases, the ability to secure a profitable property quickly or the savings from avoiding lengthy documentation processes can offset the higher rates.

Bigger down payments tie up capital: No-doc loans typically require 25-30% down payments compared to 20-25% for traditional bank loans. This higher equity requirement ties up more capital in each deal, potentially limiting an investor's ability to acquire multiple properties.

The larger down payment serves as additional security for the lender and compensates for the reduced documentation. While this increases the capital requirements for each deal, it also means investors have more equity in their properties, providing better protection against market downturns.

Origination and exit fees can add 1-3% to deal costs: No-doc loans often include origination fees, processing fees, and sometimes prepayment penalties that can add significant costs to the transaction. These fees can range from 0.5% to 2% of the loan amount at origination, with additional fees for early payoff.

Investors should carefully review all fee structures and factor them into their return calculations. Some lenders offer lower rates with higher fees, while others provide more transparent pricing with fewer add-on costs.

Many products have 3-10-year maturities or balloons—requiring a clear exit plan: Unlike traditional 20-30 year amortizing loans, many no-doc products are shorter-term bridge loans or have balloon payments. This requires investors to have clear exit strategies, whether through refinancing, sale, or business cash flow.

The shorter terms can create refinancing risk if market conditions change or if the property doesn't perform as expected. Investors should have contingency plans and ensure they can service the debt even if their primary exit strategy doesn't materialize as planned.

Some lenders impose prepayment penalties: While flexibility is often touted as an advantage of no-doc loans, some products include prepayment penalties that can limit exit options. These penalties protect lenders from interest rate risk but can be costly for borrowers who want to refinance or sell early.

Investors should carefully review prepayment terms and negotiate for flexibility when possible. Some lenders offer step-down prepayment penalties that decrease over time, while others provide penalty-free prepayment after certain periods.

Making the Strategic Decision

The decision to use no-doc financing should be based on a careful analysis of the specific deal and investment strategy. Factors to consider include:

Time sensitivity: If speed is critical to securing the property or capitalizing on market conditions, the premium for no-doc financing may be justified.

Property cash flow: The property should generate sufficient cash flow to service the higher-cost debt while still providing acceptable returns.

Exit strategy: Clear plans for refinancing or sale should be in place before taking on shorter-term no-doc financing.

Overall portfolio strategy: No-doc loans might make sense for certain deals within a larger portfolio strategy, even if they wouldn't be optimal for every acquisition.

Bottom line: pay a premium in exchange for speed and certainty. If the deal still pencils with the higher cost of funds, the trade-off makes sense. The key is understanding all costs and benefits upfront and ensuring the financing structure aligns with your investment objectives.

Exploring Financing Fit: Beyond No-Doc

Financing is a toolbox—pick the tool that matches the job.

In-House Programs You Can Tap

- DSCR loans – Qualify primarily on property cash flow; rates typically land between traditional bank debt and no-doc financing. Lenders look for a Debt Service Coverage Ratio (DSCR) of 1.25× or higher, meaning the property generates at least 25 % more income than the mortgage payment.

- Rental property loans – 30-year fixed or hybrid options for stabilized 1–4 unit portfolios, ideal for long-term holds.

- Bridge real estate loans – Short-term, interest-only capital that lets you acquire or reposition assets quickly before moving into permanent financing.

Our advisors can run side-by-side comparisons so you understand how each structure impacts cash flow and total cost of capital.

Start-Ups & First-Time Investors

No-doc isn't off the table, but expect:

- Personal guarantee and a 30 %+ down payment

- Possibly extra collateral

- Higher rates until you establish a track record

Many first-time investors partner with experienced operators, use a smaller bridge loan, or complete a single flip to prove capability before moving into lower-cost permanent debt.

Frequently Asked Questions about Commercial No-Doc Loans

Is a true "no-paperwork" loan possible?

No. The term "no-doc" is a bit of a misnomer; it really means "no income-documentation." Regulations still require lenders to verify your identity, credit, assets, and the property's value via an appraisal. You are simply skipping the step of providing tax returns and P&L statements.

How do lenders get comfortable without income docs?

Lenders mitigate risk by focusing on four key areas:

- Conservative LTV: Limiting the loan to 75% or less of the property's value ensures you have significant equity.

- Third-Party Appraisal: An independent appraisal confirms the property's market value and income potential.

- Borrower's Profile: A strong credit history and sufficient cash reserves (liquidity) demonstrate financial responsibility.

- Real Estate Experience: A track record of managing similar assets provides additional confidence.

Essentially, if the property is a strong asset and you have "skin in the game," the lender is comfortable moving forward without traditional income verification.

What credit score do I need for a commercial no-doc loan?

Most lenders look for a minimum FICO score of 650, but a score of 700+ will secure better terms and improve your chances of approval. Lenders are often more interested in your payment history on other real estate loans than on consumer debt. Recent major credit issues like bankruptcies or foreclosures can be disqualifying.

How fast can I close?

Speed is a primary advantage. While a traditional bank loan can take 45-90 days, a no-doc loan can close much faster. With all documentation in order, BrightBridge can often fund in 7-10 business days. Rush deals have even closed in as little as 3-5 days.

Can I refinance my existing commercial property with a no-doc loan?

Yes. No-doc loans are a popular option for refinancing, especially for cash-out refinances or when a traditional loan is maturing. The qualification requirements are similar to a purchase loan: strong credit, sufficient property equity, and a positive cash flow.

What happens if I can't repay the loan at maturity?

It's crucial to have a clear exit strategy from day one, such as refinancing or selling the property. Most short-term no-doc loans have extension options available, though often at a higher rate. Lenders prefer to work with borrowers on a solution rather than foreclose, but you should not rely on this. A solid plan is your best protection.

Conclusion: Is a Commercial No-Doc Loan Right for Your Investment?

A no-doc loan is a speed tool. Used on the right property, it can lock in profits that slow financing would miss; used on the wrong deal, higher carrying costs can erode returns.

Ask yourself:

- Will a quick close secure a better price or beat competitors?

- Does the property's cash flow comfortably cover the pricier debt?

- Can you place 25-30% down without straining liquidity?

If the answers are yes, let's talk. BrightBridge Realty Capital funds nationwide from our New York headquarters, offering direct decisions, competitive rates, and closings that regularly happen in under a week.

Ready to move fast? Explore your commercial financing options today and see how no-doc capital can power your next deal.