From Blueprint to Reality—Understanding Construction Loans in Connecticut

Summary

Build your CT dream home! Discover how construction loans in CT work, from application to permanent mortgage.

Why Construction Loans Are Essential for Connecticut Real Estate Investors

Construction loans in ct offer investors and homeowners a powerful way to finance new home construction or major renovations from the ground up. These short-term loans work differently from traditional mortgages—they release funds in stages as your project progresses and typically require interest-only payments during the building phase.

Key Features of Connecticut Construction Loans:

- Loan amounts: $5,000 to $10+ million depending on lender

- Down payment: 10-30% of total project cost

- Credit score: Typically 680+ required

- Loan term: 6-24 months construction phase

- Interest rates: Usually 1-2% higher than traditional mortgages

- Disbursement: Funds released in draws based on completion milestones

Connecticut's growing population (3.6 million in 2022, up from 3.4 million in 2016) and rising home prices (average $314,000 in 2022) make construction loans an attractive option for investors looking to build equity through new construction or major renovations.

Whether you're building a custom home, developing rental properties, or renovating a fixer-upper, construction loans provide the flexible financing you need to turn blueprints into profitable real estate investments.

I'm Daniel Lopez, a loan officer at BrightBridge Realty Capital with extensive experience helping Connecticut investors steer construction loans in ct for both residential and commercial projects. My background in structuring complex financing solutions has helped clients successfully complete everything from single-family builds to multi-property developments across the state.

Find more about construction loans in ct:

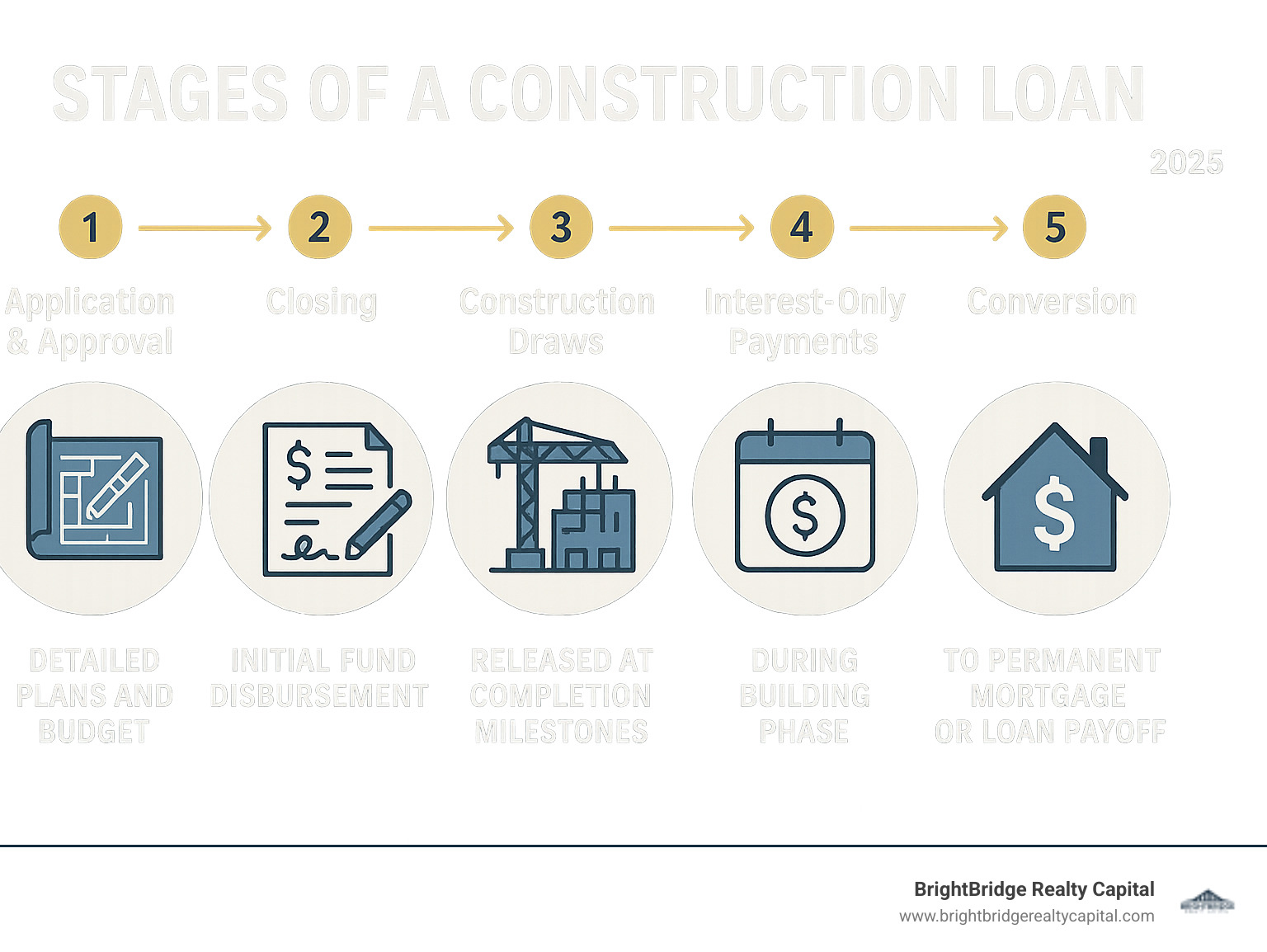

How a Construction Loan Works and Differs from a Mortgage

Think of a construction loan as the financial blueprint for your building project. While a traditional mortgage helps you buy a home that's already standing, construction loans in ct fund the exciting journey of creating something brand new from the ground up.

The differences might seem subtle at first, but they're actually quite significant. What is a construction loan? It's essentially a short-term financial partnership between you and your lender to turn your dream home into reality.

Loan purpose sets these two financing options apart immediately. Construction loans cover everything from land acquisition to the final coat of paint, while traditional mortgages simply transfer ownership of an existing property. It's like comparing funding a movie production versus buying a ticket to watch the finished film.

Disbursement method is where things get really interesting. Instead of handing you a massive check at closing (which would be pretty risky for everyone involved), construction loans release funds gradually as your project hits specific milestones. This staged approach protects both you and your lender from potential headaches down the road.

Loan terms reflect the temporary nature of construction financing. Most construction loans in ct run between 6 months and 2 years—just long enough to complete your project. Traditional mortgages, on the other hand, stretch across 15 to 30 years because they're designed for long-term homeownership.

Interest rates tend to be higher on construction loans, typically running 1-2% above conventional mortgage rates. The silver lining? You only pay interest on the amount you've actually drawn, not the full loan amount. This keeps your monthly payments manageable during the building phase.

Collateral presents another key difference. Traditional mortgages use the existing home as security, but construction loans rely on the future value of your completed project. It's like lending money based on a promise rather than something you can touch—which explains why lenders are more cautious.

Understanding Construction Loans

Construction Loan vs. Traditional Mortgage

| Feature | Construction Loan | Traditional Mortgage |

|---|---|---|

| Loan Term | 6-24 months | 15-30 years |

| Disbursement | Staged draws | Lump sum at closing |

| Interest Payments | Interest-only during construction | Principal + Interest from start |

| Collateral | Future home value | Existing property |

| Approval Process | More complex, requires detailed plans | Streamlined for existing homes |

The Draw Process Explained

The draw process is where construction loans really show their unique personality. Instead of one big money dump at the beginning, funds flow out in carefully timed releases that match your project's progress.

Draw schedules typically follow the natural rhythm of construction. Most lenders in Connecticut establish 4-6 draw periods that align with major building phases: foundation and framing, roof and exterior walls, electrical and plumbing rough-in, interior finishing, and final completion.

Project milestones act like checkpoints in a video game—you can't advance to the next level until you've completed the current one. Each draw requires specific work to be finished before funds are released, creating a built-in quality control system.

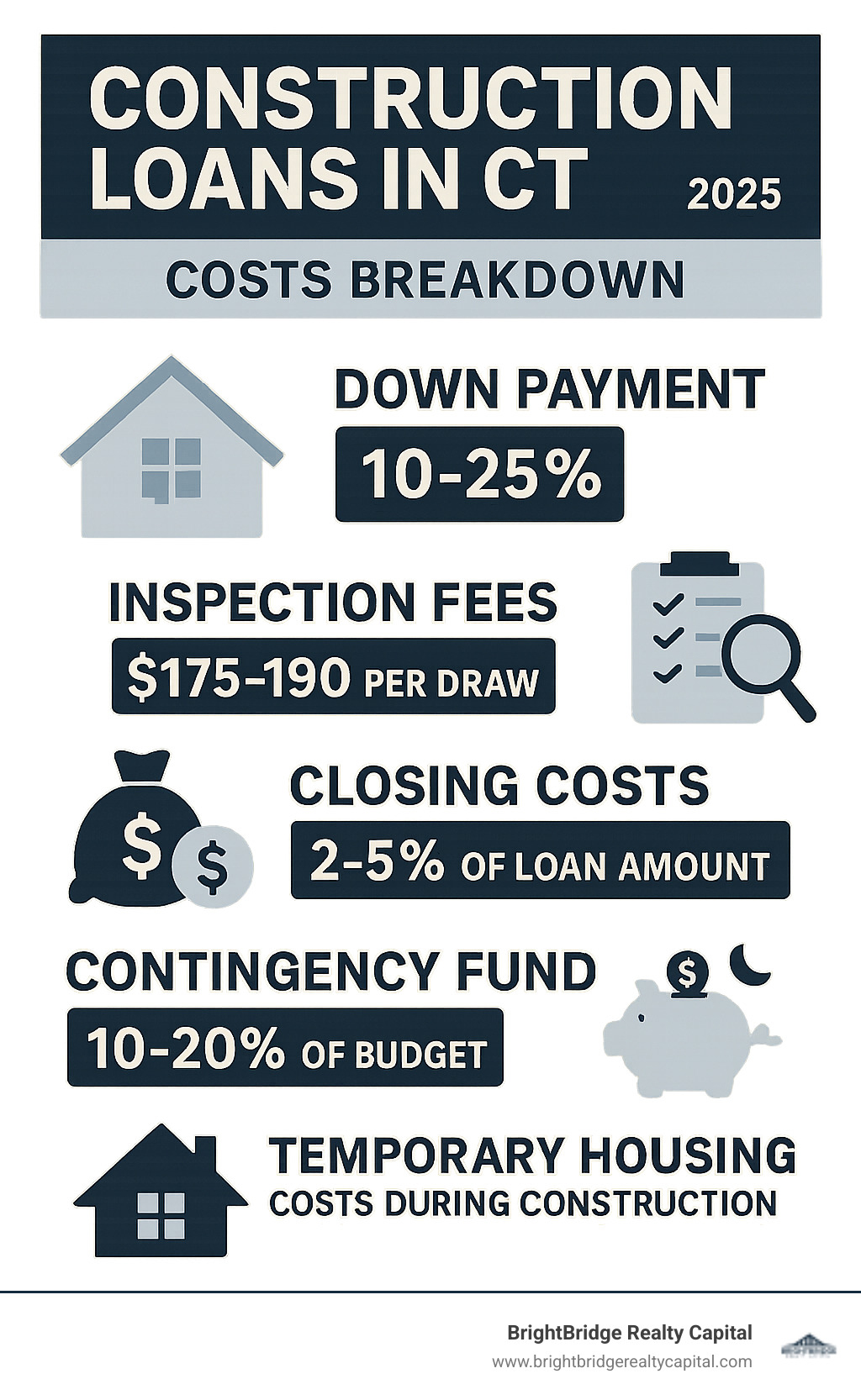

Lender inspections happen before each draw to verify that work has been completed as promised. Think of it as a friendly progress check rather than a stern examination. These inspections typically cost between $175-$190 per inspection in Connecticut, a small price for the peace of mind they provide.

Interest-only payments during construction keep your monthly costs reasonable while your home takes shape. You're only paying interest on the money that's actually been drawn and put to work, not sitting idle in an account somewhere.

Releasing funds happens once the inspection confirms that milestones have been met. Depending on your loan structure, money flows directly to your contractor or into your account, keeping the project moving forward smoothly.

Why Build a Home in Connecticut?

Connecticut's housing market tells a compelling story for anyone considering new construction. The state's population has grown steadily from 3.4 million in 2016 to 3.6 million in 2022, creating sustained demand for quality housing. This growth, combined with rising home prices, makes construction loans in ct an increasingly smart choice for both investors and homeowners.

The average cost of a home in Connecticut in 2022 is $314,000 and housing prices continue to escalate,according to CT Insider. With prices continuing to climb, building new often provides better value than purchasing existing properties—especially when you factor in the benefits of modern construction and complete customization.

Building new also means instant equity potential. When you construct efficiently with experienced contractors, your completed home's value typically exceeds the total construction cost. Plus, you get exactly what you want rather than settling for someone else's design choices.

The customization benefits alone make construction loans worthwhile. Want an open floor plan? Extra storage? A home office? Energy-efficient windows throughout? When you build new, every detail reflects your preferences and lifestyle needs.

Types of Construction Loans to Consider

One-Time Close (Construction-to-Permanent) loans have become the gold standard for most builders. This option combines construction financing and your permanent mortgage into a single loan with just one closing. After construction completes, the loan automatically converts to a traditional mortgage—no second application, no additional paperwork headaches.

Two-Time Close (Construction-Only) loans work differently. You get construction financing first, then arrange separate permanent financing after completion. While this approach offers more flexibility in choosing your permanent lender, it means two closings and potentially higher overall costs.

Government-Backed Loans can significantly reduce your upfront costs. FHA construction loans start at just 3.5% down, while VA construction loans can require as little as 0% down for eligible veterans. These programs make homeownership more accessible for qualifying borrowers.

Renovation Loans serve a different purpose—major renovations rather than ground-up construction. Programs like FHA 203(k) loans roll project costs into your overall mortgage, requiring only one application and closing.

Advantages and Disadvantages of Building

Building your dream home comes with clear advantages, but it's important to understand the challenges too.

On the positive side, you get a custom home built exactly to your specifications. Every room layout, finish choice, and feature reflects your vision. All your new appliances come with warranties, reducing maintenance headaches for years. Modern energy efficiency standards mean lower utility bills and better comfort year-round.

However, building takes patience. The longer process typically requires 6-18 months compared to 30-45 days for existing home purchases. Cost overruns can happen when unexpected issues arise or you decide to upgrade materials mid-project.

Construction loans also carry higher initial interest rates than traditional mortgages due to increased lender risk. And if you don't currently own a home, you'll need temporary housing during construction—an additional expense to factor into your budget.

Despite these challenges, many Connecticut residents find building new worth the investment, especially in today's competitive housing market.

Qualifying for Construction Loans in CT

Qualifying for construction loans in ct requires meeting stricter requirements than traditional mortgages. Lenders view construction loans as higher risk since there's no existing collateral, making thorough borrower and project evaluation essential.

Lender Requirements: Construction lenders evaluate three main areas: borrower qualifications, project viability, and builder credentials. Each must meet specific standards before loan approval.

Borrower Qualifications: Your financial strength determines loan approval and terms. Strong credit, stable income, and adequate cash reserves are essential.

Project Viability: Lenders need detailed plans, realistic budgets, and professional appraisals to ensure the project makes financial sense.

Builder Vetting: Most lenders require licensed general contractors with proven track records and proper insurance coverage.

Borrower Eligibility for construction loans in ct

Credit Score: Most Connecticut lenders require credit scores of 680-720+. Higher scores open up better rates and terms.

Down Payment: Expect to put down 10-25% of the total project cost. Some lenders offer 10% down options, while others require 20-30% depending on loan amount and borrower strength.

Debt-to-Income Ratio: Keep your debt-to-income ratio under 43-45%. This includes the projected mortgage payment on your new home.

Cash Reserves: Lenders generally want to see 2-6 months of mortgage payments in reserves beyond your down payment. This provides a safety net for unexpected costs.

Stable Income: Demonstrate consistent employment and income history. Self-employed borrowers typically need two years of tax returns and may face additional scrutiny.

Project and Builder Approval Requirements

Detailed Blueprints: Professional architectural plans showing all construction details, materials, and specifications. Plans must meet local building codes and zoning requirements.

Comprehensive Budget: Line-item budget covering all construction costs, including materials, labor, permits, and contingencies. Budgets should include a 10-20% contingency fund for unexpected expenses.

Licensed General Contractor: Most lenders require licensed, insured contractors with proven experience. The contractor's track record, references, and financial stability all factor into approval.

Project Timeline: Realistic construction timeline, typically 6-24 months depending on project complexity. Lenders want assurance the project will complete within the loan term.

Appraisal of Future Value: Professional appraisal estimating the completed home's value. The loan amount typically can't exceed 80% of the appraised future value.

Additional Costs and Key Considerations

Building a new home in Connecticut involves more than just the construction loan amount. Smart builders plan for additional expenses that can significantly impact your total project budget and monthly cash flow during construction.

The reality of construction costs means you'll need to budget beyond your initial estimates. Material price fluctuations, unexpected site conditions, and those inevitable "while we're at it" moments can quickly add thousands to your project.

Contingency fund planning is absolutely critical. Set aside 10-20% of your construction budget for unexpected costs. This isn't pessimistic thinking—it's smart planning. Change orders, material price increases, and unforeseen issues are common in construction projects, and having this buffer keeps your project moving forward without financial stress.

Closing costs for construction loans typically run higher than traditional mortgages. Based on our research, application fees in Connecticut range from $728-$995 depending on property type and lender. These upfront costs are part of the investment in your dream home.

Permit fees vary significantly by municipality but represent a necessary expense. Building permits, impact fees, and inspection costs can range from $5,000-$25,000 for single-family homes. Your contractor should help estimate these local requirements during the planning phase.

Builder's risk insurance protects your investment during construction. This specialized insurance is typically required by lenders and costs 1-4% of the construction budget. Think of it as peace of mind while your home takes shape.

Temporary housing costs become a factor if you're selling your current home to fund construction. Factor in rent or temporary housing costs during the 6-18 month construction period. Some families choose to stay with relatives or rent short-term to minimize this expense.

Land acquisition costs can often be rolled into your construction loan if you don't already own property. However, owning land for 6+ months may qualify you for better loan terms, so timing your land purchase strategically can save money.

Home Equity Loans and Lines of Credit

Finding the Right Lender for construction loans in ct

Choosing the right lender for your construction loans in ct project makes the difference between a smooth building experience and a stressful one. Not all lenders understand construction financing, and even fewer specialize in Connecticut's unique market conditions.

Local decision-making speeds up your entire process. Choose lenders who make decisions locally in Connecticut rather than sending applications to distant corporate offices. This ensures familiarity with local market conditions, building codes, and the contractors you'll be working with.

Flexible draw schedules should match your project timeline rather than forcing you into rigid payment structures. Look for lenders offering custom draw schedules beyond standard 4-6 draw periods. Some projects need more frequent draws, while others benefit from fewer, larger disbursements.

One-closing options through construction-to-permanent loans save both time and money while locking in your permanent mortgage rate upfront. This eliminates the uncertainty of having to qualify for a second loan after construction completes.

Experience with CT market matters enormously. Select lenders with proven experience in Connecticut construction loans. They understand local contractors, building codes, seasonal construction challenges, and market conditions that affect your project's success.

Transparent fees should be clearly disclosed upfront, with no surprises during construction. Watch for inspection fees, draw fees, and extension fees that can add up during construction. Understanding these costs helps you budget accurately from the start.

At BrightBridge Realty Capital, we specialize in fast, flexible construction financing with local decision-making and competitive rates. Our streamlined process often closes loans within a week, helping you start construction quickly and avoid the delays that can derail building schedules.

Frequently Asked Questions about Connecticut Construction Loans

Let's address the most common questions we hear from clients considering construction loans in ct. These concerns come up in almost every conversation, so you're definitely not alone in wondering about these details.

Is it harder to get a construction loan than a regular mortgage?

I'll be honest with you—yes, construction loans are more challenging to qualify for than traditional mortgages. But don't let that discourage you. Understanding why helps you prepare better.

The main reason is higher risk for lenders. When you buy an existing home, the lender has a physical house as collateral. With construction loans, they're betting on something that doesn't exist yet. If your project hits major problems, there's no finished home to fall back on.

This higher risk means stricter requirements across the board. While some traditional mortgages accept credit scores as low as 580-620, construction loans typically want 680-720+. Down payments jump from 3-5% to 10-25%, and lenders prefer lower debt-to-income ratios.

You'll also need more documentation. Beyond your financial information, lenders want detailed blueprints, comprehensive budgets, contractor credentials, and realistic timelines. It's like applying for a business loan and mortgage combined.

The good news? Once you understand these requirements, preparing becomes straightforward. We help clients organize everything needed to present a strong application that gets approved quickly.

What happens if construction goes over budget or past the deadline?

Construction delays and cost overruns happen more often than anyone likes to admit. Even the best contractors face unexpected challenges like weather delays, material shortages, or surprise foundation issues.

Your contingency fund is your first line of defense. This 10-20% buffer handles most unexpected costs without drama. Smart builders always include this cushion because they know surprises are part of construction.

When costs exceed your contingency, loan modifications become necessary. This means going back to your lender with updated budgets and requesting additional funds. It requires new underwriting, but experienced lenders handle these requests regularly.

For timeline extensions, submit a written request explaining the delay and providing a realistic new completion date. Most lenders understand that construction schedules can shift due to weather, permit delays, or material availability. Extension fees typically range from 0.25-1% of the loan amount.

Here's where choosing the right contractor makes all the difference. Experienced builders with solid track records rarely have major delays or cost overruns. They've seen it all before and plan accordingly. This is why lenders scrutinize contractor credentials so carefully during approval.

Can I use a construction loan to purchase the land?

Absolutely! This is one of the most powerful features of construction loans, and many clients don't realize it's possible.

Most construction loans can include land acquisition costs in the total loan amount. This means one application, one approval, and one closing for your entire project. You're not juggling separate land loans and construction financing.

If you already own suitable land, its value often counts toward your down payment. This can significantly reduce the cash you need upfront. For example, if you own $50,000 worth of land and need a $200,000 construction loan, that land might cover your entire 25% down payment.

Loan-to-value calculations get interesting here. Lenders look at the land's current value plus the projected value of your completed home. This total determines how much they'll lend and what terms you'll receive.

One-time closing benefits really shine with land purchases. Instead of paying closing costs twice—once for land, once for construction—you handle everything together. This saves thousands in fees and simplifies the entire process.

One tip: if you're shopping for land, owning it for 6+ months before applying for construction financing often gets you better loan terms. Lenders see this as reduced risk since you're more committed to the project.

Conclusion: Your Path to a New Connecticut Home

Building your dream home in Connecticut doesn't have to feel overwhelming. Construction loans in ct provide a clear path forward, even in today's competitive market where average home prices have reached $314,000 and continue climbing.

The beauty of construction financing lies in its flexibility. While traditional mortgages limit you to existing inventory, construction loans let you create exactly what you want—from the perfect kitchen layout to energy-efficient features that save money for years to come.

Success starts with solid planning. Before you even think about applying, spend time developing detailed blueprints and realistic budgets. Choose your contractor carefully—their experience and track record directly impact your project's success. Lenders don't just evaluate you; they evaluate your entire project team.

Your financial preparation matters too. Aim for a credit score above 680, save for that 10-25% down payment, and keep your debt-to-income ratio low. These steps not only improve your approval chances but also secure better rates and terms.

The right lender makes all the difference. Look for someone who understands Connecticut's unique market, offers flexible draw schedules, and makes decisions locally. You want a partner who can move quickly when opportunities arise, not someone who'll slow down your timeline with endless bureaucracy.

Don't forget the hidden costs. Budget for that 10-20% contingency fund, temporary housing expenses, and those inspection fees that add up over time. Planning for these expenses upfront prevents stressful surprises later.

Connecticut's growing population and rising home values create a perfect storm of opportunity for smart builders. Whether you're constructing a custom family home or developing investment properties, construction loans in ct provide the financial foundation to turn your vision into reality.

At BrightBridge Realty Capital, we've helped countless Connecticut builders steer this process successfully. Our fast closings—often within a week—and direct lending approach eliminate the delays and complications that plague traditional financing.

Your new Connecticut home is closer than you think. With proper planning, the right team, and flexible financing, you can break ground on your future sooner than you imagined.

https://www.brightbridgerealtycapital.com/ground-up-construction