Financiamiento de inversiones inmobiliarias: cómo comenzar

Summary

Explore opciones de financiación de inversiones inmobiliarias, consideraciones clave y consejos para que los principiantes obtengan las mejores soluciones de financiación.

Financiación de inversiones inmobiliarias es crucial para aquellos deseosos de sumergirse en la adquisición de propiedades pero que no están seguros de por dónde empezar con las opciones de financiación. Si usted es un inversor experimentado que busca ampliar una cartera de alquileres o un recién llegado que busca vender propiedades rápidamente, comprender sus opciones de financiación puede cambiar las reglas del juego.

Para comprender rápidamente las opciones de financiación de inversiones inmobiliarias, considere estas rutas:

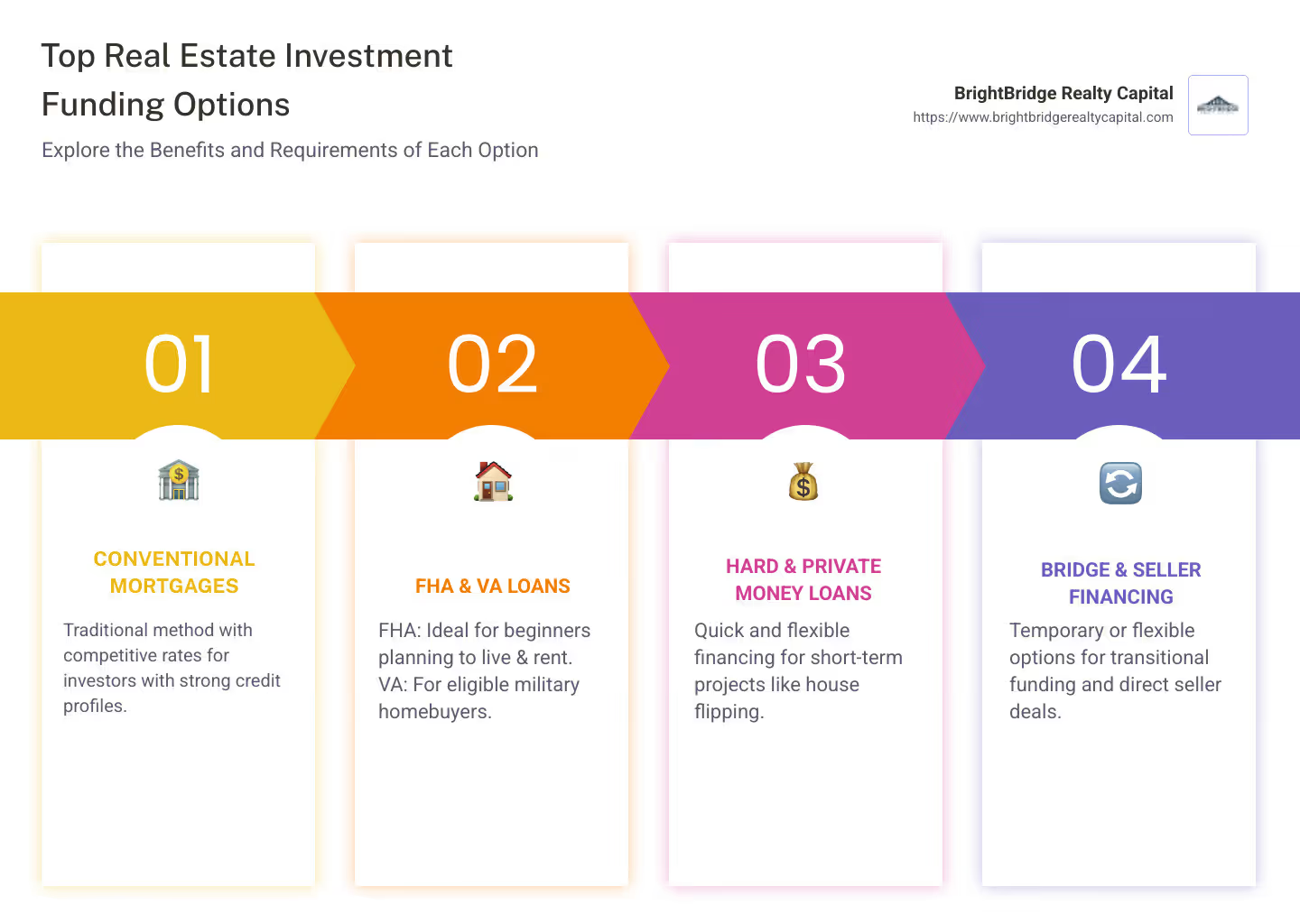

- Hipotecas convencionales: Método tradicional con excelentes tasas para inversores con crédito sólido.

- Préstamos de la FHA: Ideal para nuevos inversores que deseen vivir y alquilar en el lugar.

- Préstamos VA: Perfecto para compradores militares elegibles que planean vivir en la propiedad.

- Préstamos de dinero fuerte: Financiamiento rápido con retorno a corto plazo, adecuado para proyectos de inversión.

- Préstamos de dinero privados: Plazos flexibles a través de prestamistas privados.

- Préstamos puente: Financiamiento temporal para la transición entre inversiones.

- Financiamiento del vendedor: Financiamiento directo de vendedores con potencial flexibilidad.

- Soluciones personalizadas: Financiamiento personalizado para satisfacer necesidades de inversión únicas.

Cada opción tiene sus propios beneficios y requisitos, y elegir la correcta puede ser la clave para una inversión exitosa.

El sector inmobiliario no se trata sólo de comprar y vender propiedades: se trata de tomar decisiones estratégicas de financiación para aprovechar las oportunidades de manera eficaz.

Comprensión de la financiación de inversiones inmobiliarias

Financiación de inversiones inmobiliarias Puede resultar abrumador al principio, pero comprender los conceptos básicos puede ayudarle a tomar decisiones inteligentes. Analicemos los componentes clave: propiedades de inversión, opciones de financiación y deuda apalancada.

Propiedad de inversión

Las propiedades de inversión son activos inmobiliarios adquiridos para generar ingresos mediante el alquiler, el arrendamiento o la venta con fines de lucro. Ofrecen una variedad de beneficios:

- Flujo de caja estable: Al alquilar propiedades, los inversores pueden obtener ingresos constantes. Por ejemplo, las propiedades en áreas de alta demanda pueden proporcionar un flujo de ingresos confiable.

- Valorización de la propiedad: Históricamente, los bienes raíces se aprecian con el tiempo. Desde 1963, los precios de las viviendas en Estados Unidos han aumentado más del 5,5% anual, superando la inflación del 3,9% anual.

- Beneficios fiscales: Los inversores pueden deducir los intereses hipotecarios, los impuestos sobre la propiedad y la depreciación, lo que reduce la renta imponible. Estrategias como las bolsas 1031 pueden aplazar los impuestos sobre las ganancias de capital.

- Diversificación de carteras: Los bienes raíces a menudo se comportan de manera diferente a las acciones, proporcionando un amortiguador durante las caídas del mercado de valores.

Opciones de financiación

Elegir la opción de financiación adecuada es crucial. A continuación se muestran algunos métodos comunes:

- Hipotecas convencionales: Estos son los elegidos por muchos inversores con buen crédito. Requieren un pago inicial más alto pero ofrecen tarifas competitivas.

- Préstamos de dinero fuerte: Estos son préstamos a corto plazo ideales para cambios rápidos de propiedad. Tienen tasas de interés más altas pero brindan un acceso rápido a los fondos.

- Préstamos de dinero privados: Ofrecidos por prestamistas privados, estos préstamos son flexibles pero pueden tensar las relaciones personales. Se basan en la confianza y en acuerdos personales.

- Préstamos sobre el valor de la vivienda y HELOC: Estos aprovechan el valor líquido de su vivienda actual. Si bien ofrecen tasas más bajas, corren el riesgo de una ejecución hipotecaria si no se cumplen los pagos.

- Financiamiento del vendedor: El vendedor actúa como prestamista, permitiendo a los compradores pagarle directamente. Esto puede ser flexible pero implica riesgos como el incumplimiento del posible comprador.

Apalancamiento de la deuda

El apalancamiento es una herramienta poderosa en la inversión inmobiliaria. Le permite controlar un activo de alto valor con una cantidad relativamente pequeña de su propio dinero. La clave es utilizar sabiamente los fondos prestados para aumentar los rendimientos potenciales:

- Controle más con menos: Al utilizar préstamos, puede comprar más propiedades que si dependiera únicamente del efectivo.

- Generar capital: A medida que los inquilinos pagan el alquiler, ayudan a pagar la hipoteca, lo que aumenta su valor líquido con el tiempo.

- Gestión de riesgos: Si bien el apalancamiento puede amplificar la rentabilidad, también aumenta el riesgo. Si el valor de la propiedad baja, usted podría deber más de lo que vale la propiedad.

Comprender estos elementos de financiación de inversiones inmobiliarias puede sentar las bases para inversiones inmobiliarias exitosas. A continuación, profundizaremos en las mejores opciones de financiación disponibles para inversores inmobiliarios.

Las 10 mejores opciones de financiación de inversiones inmobiliarias

Cuando se trata de financiación de inversiones inmobiliarias, elegir la opción de financiación adecuada es clave para maximizar su rentabilidad y minimizar los riesgos. Aquí hay un resumen de las diez mejores opciones:

1. Hipotecas convencionales

Las hipotecas convencionales son una opción popular para inversores con un historial crediticio sólido. Por lo general, requieren un pago inicial del 20 % y ofrecen tasas de interés competitivas. Estos préstamos son mejores para comprar viviendas unifamiliares o pequeñas unidades multifamiliares. Puede obtener estos préstamos a través de bancos o cooperativas de crédito.

2. Préstamos de la FHA

FHA loans are great for new investors looking to start with a multi-family property. They allow for a lower down payment (as low as 3.5%) and have flexible credit requirements. However, you must live in one of the units as your primary residence. Esto hace que los préstamos de la FHA sean ideales para piratear viviendas.

3. Préstamos VA

Reserved for military veterans and service members, VA loans offer 0% down payments and no private mortgage insurance. Like FHA loans, you need to live on the property. They're perfect for eligible military buyers looking to invest in a property they can reside in while renting out other units.

4. Préstamos de dinero fuerte

Hard money loans are short-term loans provided by private lenders. They're based more on the property's value than the borrower's creditworthiness. These loans are ideal for quick fix-and-flip projects due to their fast approval process but come with higher interest rates.

5. Préstamos de dinero privados

Private money loans come from individuals or private companies willing to lend based on a personal relationship. They offer flexibility but can strain relationships if not managed well. These are best for investors who have access to wealthy acquaintances or family members willing to invest.

6. Préstamos puente

Bridge loans are temporary loans used to bridge the gap between buying a new property and selling an existing one. They have higher interest rates and shorter terms, making them suitable for investors needing quick access to funds for a new purchase while waiting for another property to sell.

7. Préstamos para bienes raíces comerciales

Commercial loans are used for financing multi-unit residential or commercial properties. They require higher credit scores and down payments. These loans are ideal for investors looking to purchase large apartment complexes or commercial spaces.

8. Préstamos sobre el valor de la vivienda y HELOC

These loans allow you to borrow against the equity in your home. Home equity loans provide a lump sum, while HELOCs offer a revolving line of credit. They're great for investors looking to fund additional property purchases but come with the risk of foreclosure if payments aren't made.

9. Financiamiento del vendedor

En la financiación del vendedor, el vendedor actúa como prestamista, lo que permite al comprador realizarle pagos directamente. This can be a flexible option for buyers who may not qualify for traditional loans. However, it carries risks, such as potential default by the buyer.

10. Soluciones de financiación personalizadas

Para aquellos que buscan soluciones personalizadas, empresas como BrightBridge Realty Capital ofrecer opciones de financiación personalizadas. These solutions are designed to align with your specific investment strategy and growth plans, providing the flexibility needed to expand your portfolio.

Elegir lo correcto financiación de inversiones inmobiliarias option depends on your financial situation, investment goals, and risk tolerance. Next, we'll discuss key considerations to keep in mind when selecting your financing option.

Real Estate Investment Funding: Key Considerations

Al sumergirse en financiación de inversiones inmobiliarias, there are three critical factors to keep in mind: down payments, credit requirements, and interest rates. Understanding these can make or break your investment journey.

Pagos iniciales

Most financing options for investment properties require a significant down payment. Conventional mortgages, for instance, typically demand at least 20% down. This is because lenders view investment properties as riskier than primary residences.

However, some options like FHA loans allow for lower down payments, as low as 3.5%, but come with the condition that you must live in one of the units. VA loans even offer 0% down payments for eligible veterans, providing a unique opportunity for those who've served in the military.

Requisitos de crédito

Su puntaje crediticio juega un papel muy importante en financiación inmobiliaria. Higher scores open doors to better interest rates and loan terms. For conventional loans, you'll generally need a credit score of at least 620. But keep in mind, the higher your score, the more favorable your terms will be.

Hard money loans are an exception as they focus more on the property's value than your credit score. This makes them appealing for quick deals, but they come with higher interest rates.

Tasas de interés

Interest rates can significantly impact your investment's profitability. These rates vary based on the loan type and your creditworthiness. Conventional loans usually offer competitive rates, but they can fluctuate based on market conditions.

Hard money loans, while offering quick access to funds, come with notably higher interest rates. This makes them suitable for short-term projects, like house flips, where you can repay quickly.

Equilibrar sus opciones

Finding the right balance between down payments, credit requirements, and interest rates is key. It’s about aligning these factors with your financial situation and investment strategy. For instance, if you have a strong credit score and sufficient savings, a conventional mortgage could be your best bet. On the other hand, if you're looking for flexibility, exploring options like private money loans or seller financing might be worthwhile.

By understanding these key considerations, you can make informed decisions that align with your investment goals. Next, we'll explore how beginners can steer real estate investment funding with strategies like house hacking and rental properties.

Financiamiento de inversiones inmobiliarias para principiantes

Comenzando tu viaje en financiación de inversiones inmobiliarias puede resultar abrumador. But don't worry, there are strategies designed for beginners that can make this process smoother and more accessible.

Hackeo de casas

House hacking is a popular entry point for new investors. It involves buying a multi-unit property, living in one unit, and renting out the others. This strategy allows you to use rental income to offset your mortgage and other expenses.

For example, you might use an FHA loan, which requires as little as a 3.5% down payment, to purchase a duplex. Vives en una mitad y alquilas la otra. This not only makes homeownership more affordable but also provides a taste of property management without the full commitment of a standalone rental property.

Propiedades de alquiler

Investing in rental properties is another way to enter the real estate market. This approach involves purchasing a property with the intention of renting it out to tenants. Rental properties can offer a steady income stream and potential for long-term appreciation.

To fund rental properties, beginners often use conventional mortgages. These loans are designed for properties that are not your primary residence and typically require a 20% down payment. However, the steady rental income can help cover monthly mortgage payments and other expenses, making it a viable option for those looking to build wealth over time.

Soluciones de financiación personalizadas

Sometimes, traditional funding routes may not fit your needs. That's where customized financing solutions come in. These options are custom to your specific financial situation and investment goals.

For instance, BrightBridge Realty Capital offers customized financing solutions that can help new investors steer the complexities of real estate funding. Whether it's through flexible loan terms or innovative funding strategies, these solutions can provide the support you need to get started.

By starting with house hacking or rental properties, and exploring customized financing options, you can ease into real estate investment. These strategies not only make property investment more accessible but also offer valuable learning experiences for future ventures.

Next, we'll dive into frequently asked questions about real estate investment funding, including the best ways to finance an investment and the potential of real estate crowdfunding.

Frequently Asked Questions about Real Estate Investment Funding

What is the best way to finance a real estate investment?

When it comes to financing a real estate investment, hipotecas convencionales suelen ser la opción preferida por muchos inversores. They offer competitive interest rates and long repayment terms, typically between 15-30 years. With a conventional mortgage, you can secure up to 80% of the property's purchase price, leaving you with a 20% down payment. This option is ideal for investors with strong credit and stable income.

However, if traditional methods don't suit your needs, soluciones de financiación personalizadas podría ser la respuesta. These solutions are custom to your specific financial situation and investment goals. BrightBridge Realty Capital, for instance, offers flexible loan terms and innovative funding strategies to help you find the best fit for your investment.

¿Es el crowdfunding inmobiliario una buena inversión?

Real estate crowdfunding has gained popularity as a way for smaller investors to enter the market with less capital. A través de plataformas de inversión inmobiliaria, multiple investors pool their money to fund real estate projects. This approach allows you to invest in larger properties without bearing the full financial burden.

Crowdfunding offers several benefits, such as diversification and access to professional management. However, it's important to consider potential risks like lower liquidity and platform fees. For those interested in passive investment opportunities, real estate crowdfunding can be a viable option. Just be sure to research platforms thoroughly and understand the terms before investing.

How do REITs compare to other real estate investments?

Fideicomisos de inversión inmobiliaria (REIT) provide a way to invest in real estate without directly owning property. They invest in income-producing real estate and distribute 90% of their taxable income as dividends to shareholders. This makes REITs attractive for investors seeking regular income.

Hay dos tipos principales de REIT: REIT de acciones y REIT hipotecarios. Equity REITs own and manage real estate properties, while mortgage REITs lend money to real estate owners or invest in mortgage-backed securities.

Compared to direct property ownership, REITs offer greater liquidity since they trade on major stock exchanges. They also provide diversification and professional management. However, REITs primarily generate income through dividends, so they may not be ideal for investors looking for capital appreciation.

For those interested in steady income and easy access to the real estate market, REITs can be a great addition to an investment portfolio.

Conclusión

In real estate investment, finding the right funding option is crucial. BrightBridge Realty Capital se destaca ofreciendo soluciones de financiación personalizadas que atienden las necesidades únicas de cada inversor. Whether you're flipping houses, building from the ground up, or expanding your rental portfolio, BrightBridge has you covered.

One of the key advantages of working with BrightBridge is their commitment to financiación rápida. With fast closings, often within a week, they ensure you can seize investment opportunities without delay. Their direct lending approach eliminates intermediaries, providing competitive rates and a seamless process.

Al elegir BrightBridge Realty Capital, no solo obtiene un préstamo; you're partnering with a team that understands your investment strategy and is dedicated to helping you succeed. If you're ready to explore custom financing options that align with your goals, visite BrightBridge Realty Capital hoy.